The $491 Million Sleight of Hand

MongoDB: MDB

On February 3, 2026, a tremor hit the software sector, and MongoDB (MDB) found itself at the epicentre, shedding nearly 10% of its value in a single session. To the casual observer, it looked like collateral damage - a “sympathy move” following cautious guidance from the titans at Microsoft and SAP. But if you look closer at the plumbing of the enterprise, specifically Line 11 of the FY2025 Statement of Cash Flows, a more curious story emerges.

That line represents Stock-Based Compensation (SBC).

In 2025, MongoDB handed out $491.2 million in equity to its people. To put that in perspective, the company’s total Free Cash Flow was just $121 million.

It’s a peculiar math: for every dollar of cash the business generated for the “house,” it handed nearly four dollars in new chips to the dealers. This is the central tension of the modern software insurgent. MongoDB has built the most elegant, flexible “document” database in the world, yet the shareholders are currently paying a massive premium for the privilege of being diluted.

The System: Why Databases Are the Ultimate Sticky Note

The market isn’t a graph of “cloud growth”; it’s a system of technical debt and path dependency. In the old world, data lived in rigid SQL tables, think of it like a filing cabinet where every folder must be exactly the same size. MongoDB’s “NoSQL” document model is more like a digital folder that expands and adapts.

Once a developer builds an application’s brain on MongoDB, moving it is an architectural nightmare. This creates a “Switching Cost” moat. However, the system is under siege. The cloud giants, AWS and Azure, are no longer just hosts; they are competitors, offering their own “good enough” versions (DynamoDB and Cosmos DB) bundled into their existing contracts.

The Analytical Deep Dive (The Numbers)

To grasp the mystery inside MongoDB, we have to look at the gap between what management calls “profit” and what actually hits the bank account.

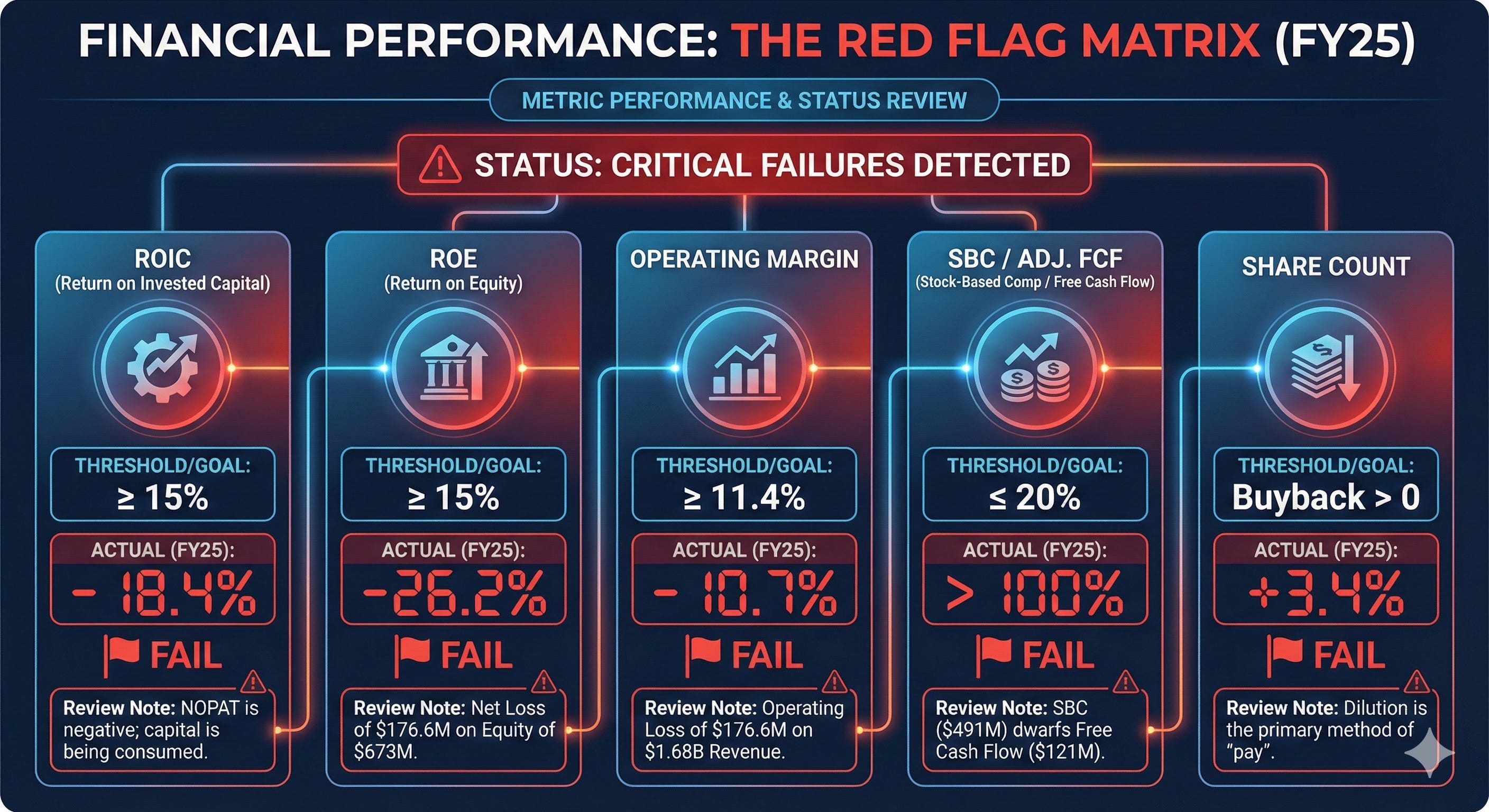

Table 1: The Red Flag Matrix (Quality & Safety)

The investigation reveals a paradox. Revenue is screaming higher (up 31% YoY), and Gross Margins are a pristine 73%. But the bottom line is a sea of red.

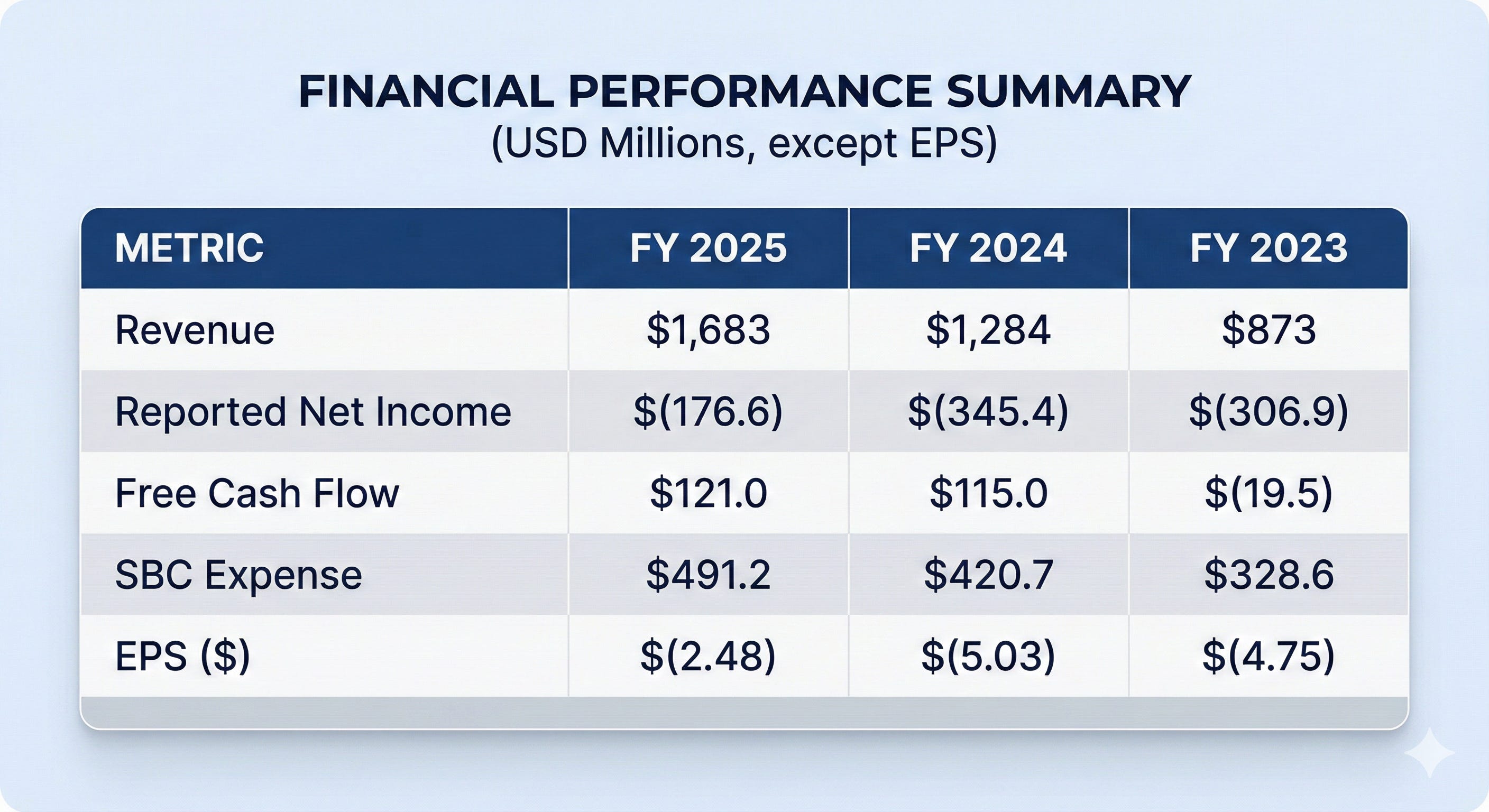

Table 2: Financial Performance History (USD Millions)

Management points to “Adjusted EBITDA” of $62.6 million as a sign of success. But that number only exists because they added back that $491 million in stock grants. In the Lewis-esque reality of “who is winning,” the employees are winning, while the equity holders are seeing their slice of the pie shrink by 3.4% every year through dilution.

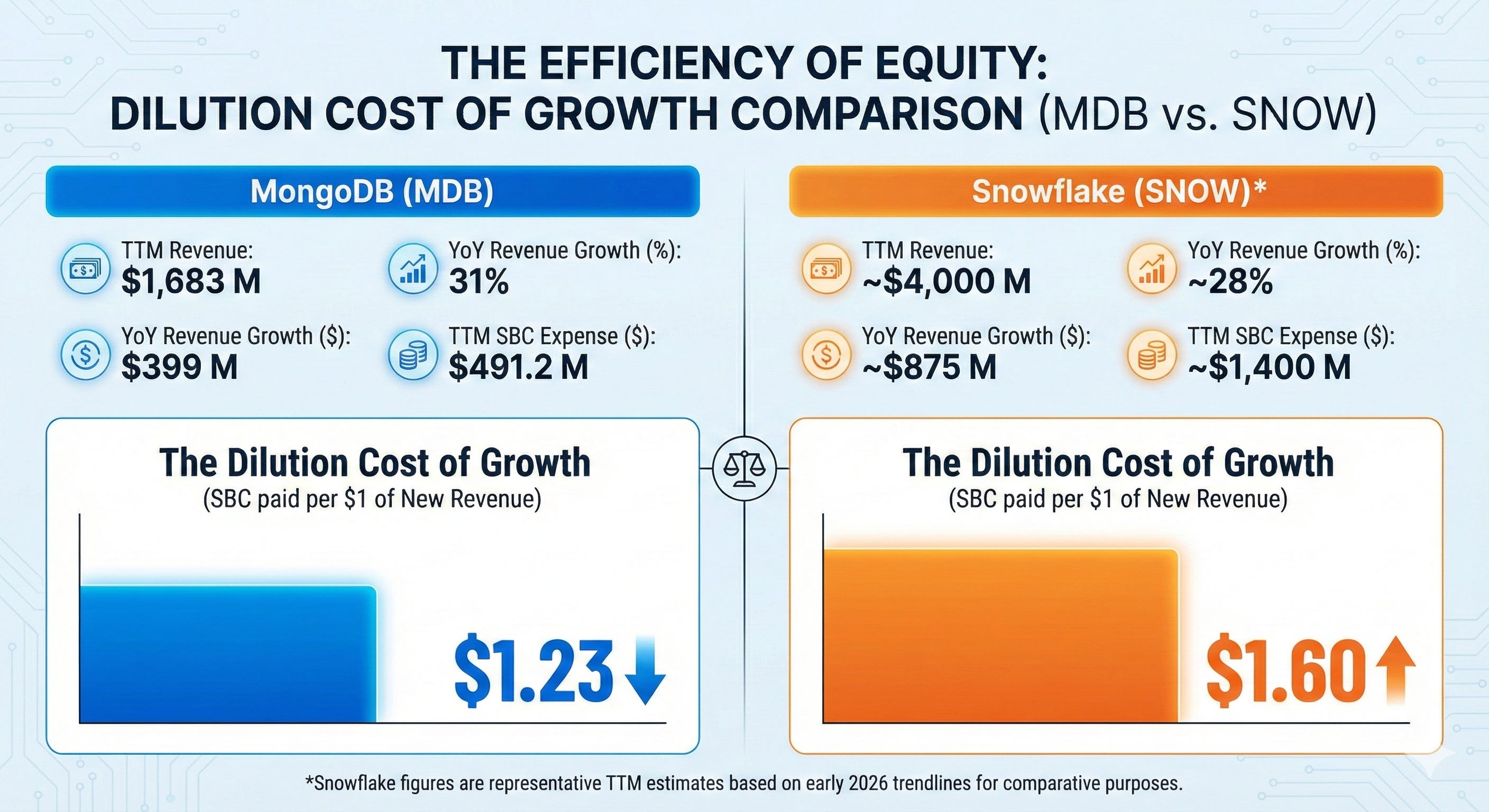

The Sector Epidemic: A Peer Review (Enter Snowflake)

Is this just a MongoDB problem? Or is it a systemic infection? To find the answer, we have to bring in a control group: Snowflake (SNOW).

The narrative of the modern data stack is no longer about who can store the most bytes; it is about who can generate the most cash without handing it all back to the engineering department. When we compare the two, a frightening picture of the “SBC Tax” emerges.

The Intensity of the Burn:

Snowflake: In the first half of FY2026, Snowflake’s stock-based compensation sat at roughly 35% to 36% of revenue, peaking at 43% in prior periods.

MongoDB: Operates at roughly 29%.

While MongoDB is arguably the more disciplined operator. Snowflake attempts to mask this dilution through aggressive buybacks, repurchasing nearly $490 million in shares recently. This creates a “circular economy”: the company generates cash, uses that cash to buy back shares, and then issues those shares right back to employees. It is a capital allocation treadmill that keeps the share count from exploding but prevents that cash from ever reaching the “owner’s” pocket.

MongoDB, to its credit, is closer to the shore. In Q3 FY2026, its GAAP operating loss narrowed to $18.4 million, while Snowflake’s remained a cavernous $330 million.

The Bull Case: The Generative AI Tailwind

The optimist sees MongoDB as the essential “Vector” for the AI revolution. If data is the new oil, MongoDB is the most sophisticated refinery.

The Unstructured Edge: AI thrives on messy, unstructured data. MongoDB’s document model is natively suited for this, unlike the rigid SQL databases of the 1990s.

The Atlas Engine: Their Cloud-as-a-Service (Atlas) is growing at a clip that suggests they are out-innovating the legacy players.

The Pivot to Profit: The Bull argues that the massive R&D spend ($568M) and Sales spend ($767M) are temporary land-grabs. Once they own the developer’s heart, they can turn off the spending tap and the cash will flood in.

The Bear Case: The Dilution Treadmill

The skeptic looks at the valuation and sees a story that requires a miracle to end well. At the current price of $336.08, MongoDB trades at a 200.8x Price-to-FCF multiple.

The SBC Debt Bomb: If we treat stock compensation as a real expense - which it is, because it dilutes your ownership - the “Fully Adjusted FCF” is actually negative $370 million.

The Commodity Trap: Cloud providers are making it easier to use their native databases. Why pay for MongoDB Atlas when AWS can give you a “good enough” version for 30% less on the same bill?

Valuation Gravity: Historically, MongoDB has traded at an average P/FCF of 250x, but that was in a zero-interest-rate world. In today’s market, paying 200x for a company that hasn’t posted a GAAP profit is like buying a house for 200 times its annual rent.

The Buy Trigger: When the Risk Flips

There is a scenario where the narrative shifts.

The intrinsic “Medium” value of the firm sits around $332.64, strikingly close to today’s price. However, we aren’t looking for “fair.” We are looking for an edge.

The stock becomes an undeniable purchase if:

The Margin of Safety is Hit: A further retreat to the $230 - $240 range. This would price in the “SBC tax” while giving you the growth for free.

The GAAP Inflection: Management announces a definitive “burn-down” plan for SBC, reducing it to below 15% of revenue.

The Peer Arbitrage: If MDB trades at a 50% discount to SNOW on a Price/Sales basis while maintaining similar Atlas growth, the market has mispriced the relative efficiency of MongoDB’s operation.

Final Verdict

MongoDB is a world-class product currently operating as a world-class employment agency for engineers. The product has a moat, but the business hasn’t yet built a wall around its cash. While it is visibly “leaner” than its peer Snowflake, it remains a brilliant tool in a speculative wrapper. Until the dilution slows or the price reflects the true cost of that equity, the smart money waits.

The SBC-to-FCF ratio is brutal—nearly 4:1 is unsustainable for equity holders. I ran into this same issue analyzing SNOW last quarter. The comparison with Snowflake is instructive tho; at least MDB isnt burning as hard operationally. The $230-240 trigger makes sense if they actually commit to slowing dilution, but until managment signals that shift, its just hope pricing.