Why U.S. Bancorp (USB) is a Prime Target for 2026

Deep Value Analysis Banking Series

Date: December 28, 2025

Ticker: USB

Current Price: $54.99

Verdict: ⭐⭐⭐ Prime Target (Buy)

In the current market environment, finding high-quality assets trading at significant discounts is rare. Most “wonderful businesses” are priced for perfection. However, our latest quantitative analysis highlights a significant divergence between price and value in U.S. Bancorp (USB).

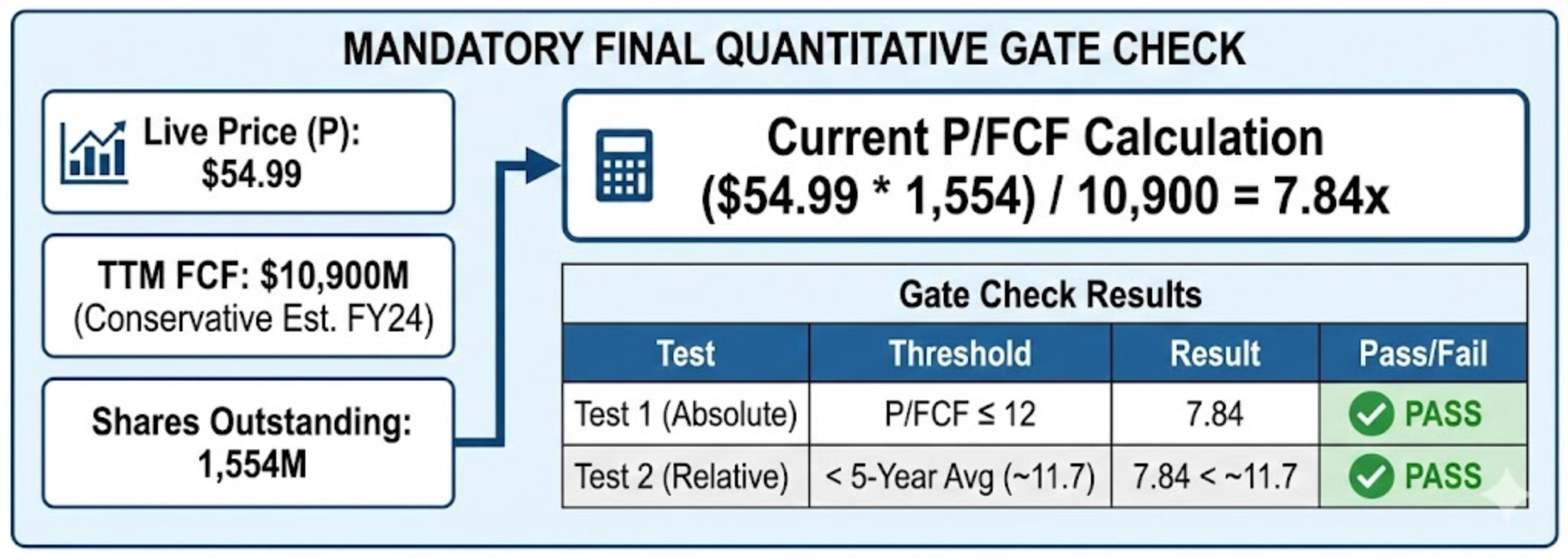

After a screen, USB has triggered a deep-value buy signal. Trading at roughly 7.8x Free Cash Flow with a durable competitive advantage and a fortress balance sheet, the stock appears significantly mispriced relative to its intrinsic earnings power.

Here is the deep-dive investment thesis.

The Business Model: A Technology Platform Disguised as a Bank

To the casual observer, U.S. Bancorp looks like a standard regional bank dependent on interest rate spreads. While traditional lending is core to its operations, this view misses the company’s most valuable differentiator: Payment Services.

USB operates a unique three-pillar model:

Consumer & Business Banking (32% of Revenue): The foundation—stable, low-cost deposits and lending.

Wealth & Corporate Banking (43% of Revenue): High-touch services for institutional and high-net-worth clients.

Payment Services (25% of Revenue): The growth engine. USB is a top-tier merchant acquirer and commercial card issuer.

Strategic Advantage: Payment services generate fee income rather than interest income. This segment is less sensitive to interest rate volatility and requires minimal capital to scale compared to lending. It effectively embeds USB into the daily operations of its business clients, creating a “sticky” ecosystem that competitors find difficult to disrupt.

The Moat: Scale and Interconnectedness

We assess USB’s competitive advantage as strong (Score: 8/10), built on two primary factors:

Cost Advantage (Scale): With $678 billion in assets, USB can sustain the $2.5 billion annual technology investment required to modernize its platforms—a spending level that smaller regional banks cannot match.

Switching Costs: The bank’s “Interconnectedness” strategy deepens client relationships. When a corporate client utilizes USB for lending, merchant processing, and corporate cards, the operational cost of switching banks becomes prohibitively high. This is reflected in the robust 14.1% growth in fee revenue reported in the most recent quarter.

Financial Health: Efficiency and Capital Discipline

Our quantitative safety screens confirm a high level of financial durability:

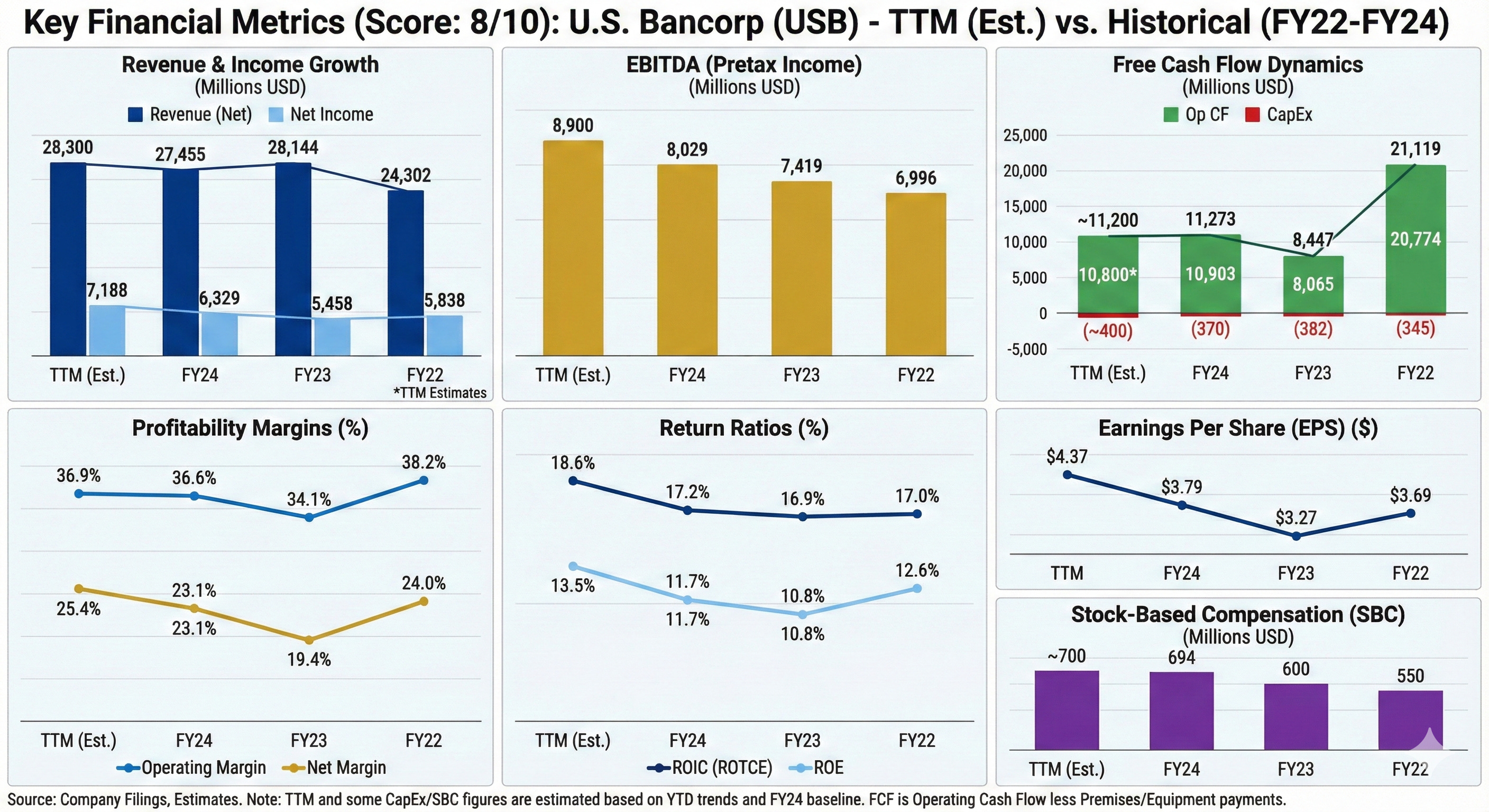

Capital Efficiency: The bank generated a Return on Tangible Common Equity (ROTCE) of 18.6% in the trailing twelve months, well above the industry standard benchmark of 15%.

Cash Quality: Cash conversion is excellent. For every $1.00 of reported Net Income, the company generates approximately $1.56 in Free Cash Flow, driven by non-cash provision expenses.

Balance Sheet Safety: The CET1 capital ratio stands at 10.9%, providing a healthy buffer above regulatory minimums.

Risk Check:

Restatements: None.

Goodwill Impairments: None.

Share Count: The company has resumed share buybacks following the successful integration of Union Bank.

The Catalyst: Leadership Continuity and ROE Focus

Market uncertainty regarding leadership has resolved. Long-time CEO Andy Cecere is transitioning to Executive Chairman, with Gunjan Kedia taking over as CEO in April 2025.

This transition is a positive catalyst. Kedia previously led the Wealth and Payment divisions—the company’s highest-growth and highest-margin segments. Furthermore, executive compensation remains heavily tied to Return on Equity (ROE), ensuring management is incentivized to prioritize capital efficiency over “growth at any cost.”

Valuation: A Significant Margin of Safety

The investment case largely rests on the current valuation disconnect.

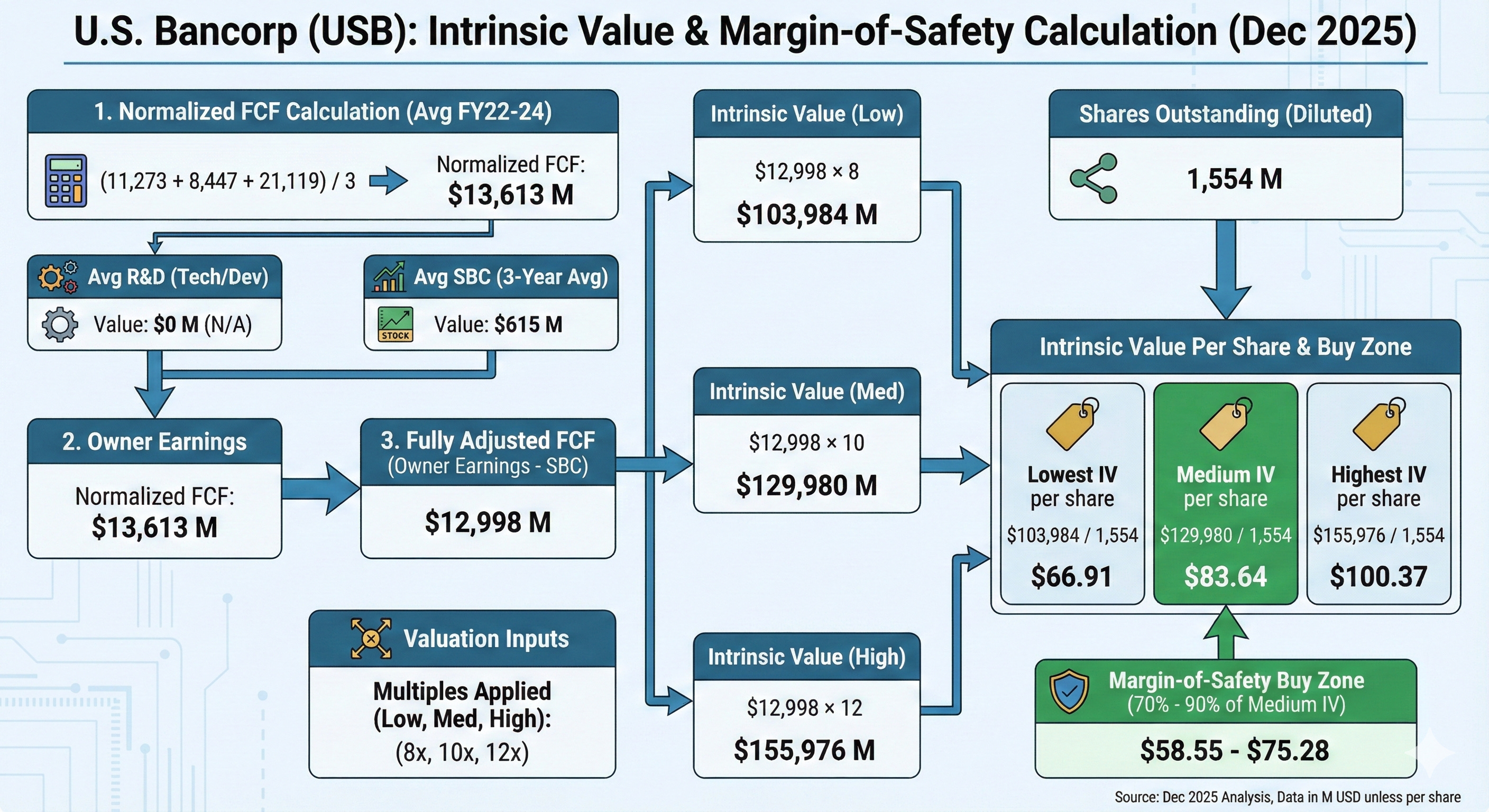

We utilized an Owner Earnings model to determine the Intrinsic Value (IV) of the stock based on normalized cash flows.

Normalized Free Cash Flow: ~$13.6 Billion

Current Market Cap: ~$85 Billion

The Multiples:

Historically, USB trades at approximately 12x Price-to-Free-Cash-Flow (P/FCF). Today, it trades at just 7.8x.

Intrinsic Value Calculation:

Applying a conservative 10x multiple to fully adjusted cash flows yields a Medium Intrinsic Value of $83.64 per share.

Current Price: $54.99

Intrinsic Value: $83.64

Implied Upside: +52%

At current levels, investors are effectively buying the business at a 34% discount to its fair value. Even under a pessimistic “low-growth” scenario, our model sets the floor value at $66.91, suggesting the downside risk is well-contained.

Risks to Monitor

Commercial Real Estate (CRE): Like the broader banking sector, USB has exposure to office commercial real estate. However, credit quality remains resilient with net charge-offs at a manageable 0.56%, and reserve levels appear prudent.

Regulatory Changes: The “Basel III Endgame” proposals could increase capital requirements for large regional banks. While USB is well-capitalized, stricter regulations could temporarily temper the pace of dividend hikes or buybacks.

Final Verdict

Ranking: ⭐⭐⭐ (Prime Target)

U.S. Bancorp offers a compelling combination of a defensive business model, a unique payments franchise, and a valuation that implies zero growth. The market has priced the stock as a distressed regional bank, ignoring its superior return on capital and fee-generation capabilities.

Action: BUY

Price Target: $83.00

Disclaimer: This analysis is for informational purposes only and does not constitute financial advice. Investors should conduct their own due diligence.