The Twenty-Seven Times Dilemma

Why the AI Party is Just Getting Started

On a cold December evening in 1996, in a ballroom in Washington D.C., Alan Greenspan, then Chairman of the Federal Reserve, stood up and delivered a speech that would become famous for two words. He looked out at an economy that was humming with the nascent promise of the internet, a new technology that was clearly going to change everything, and he wondered aloud if the stock market was suffering from “irrational exuberance.”

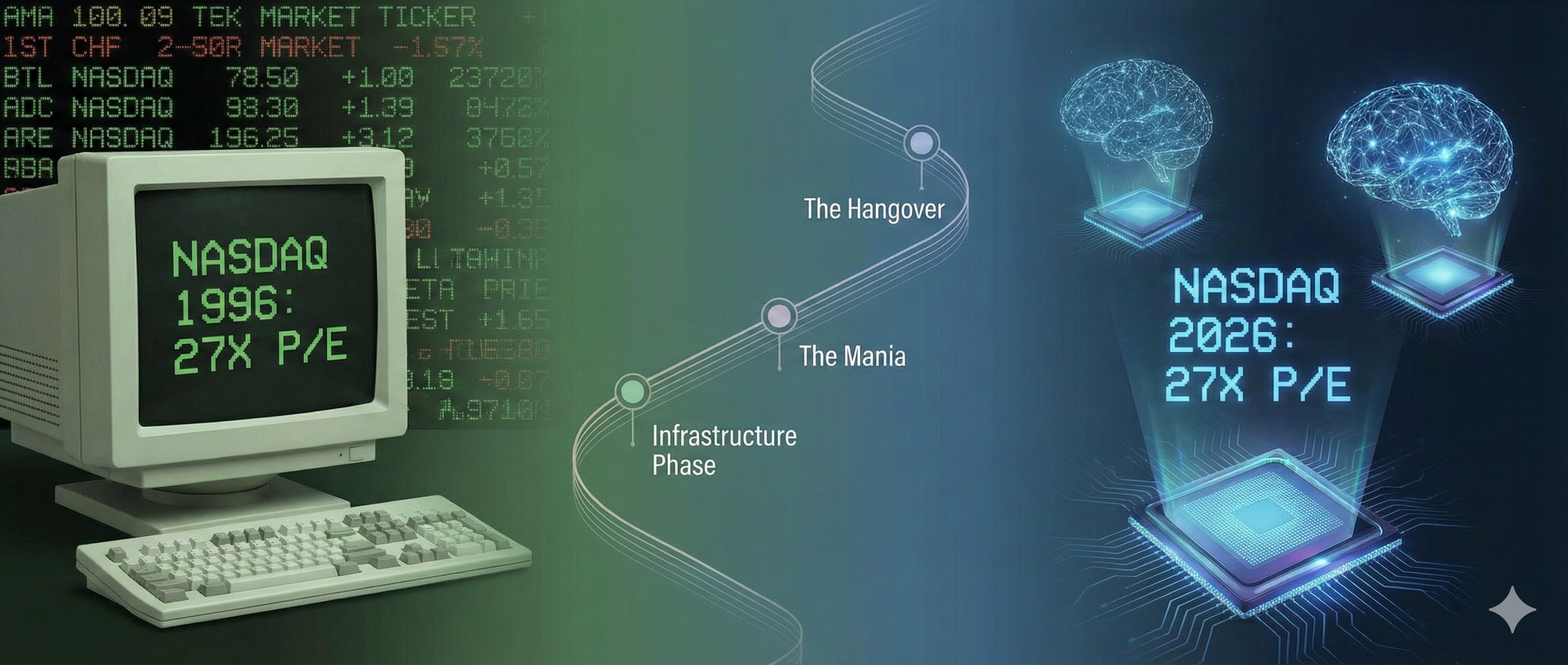

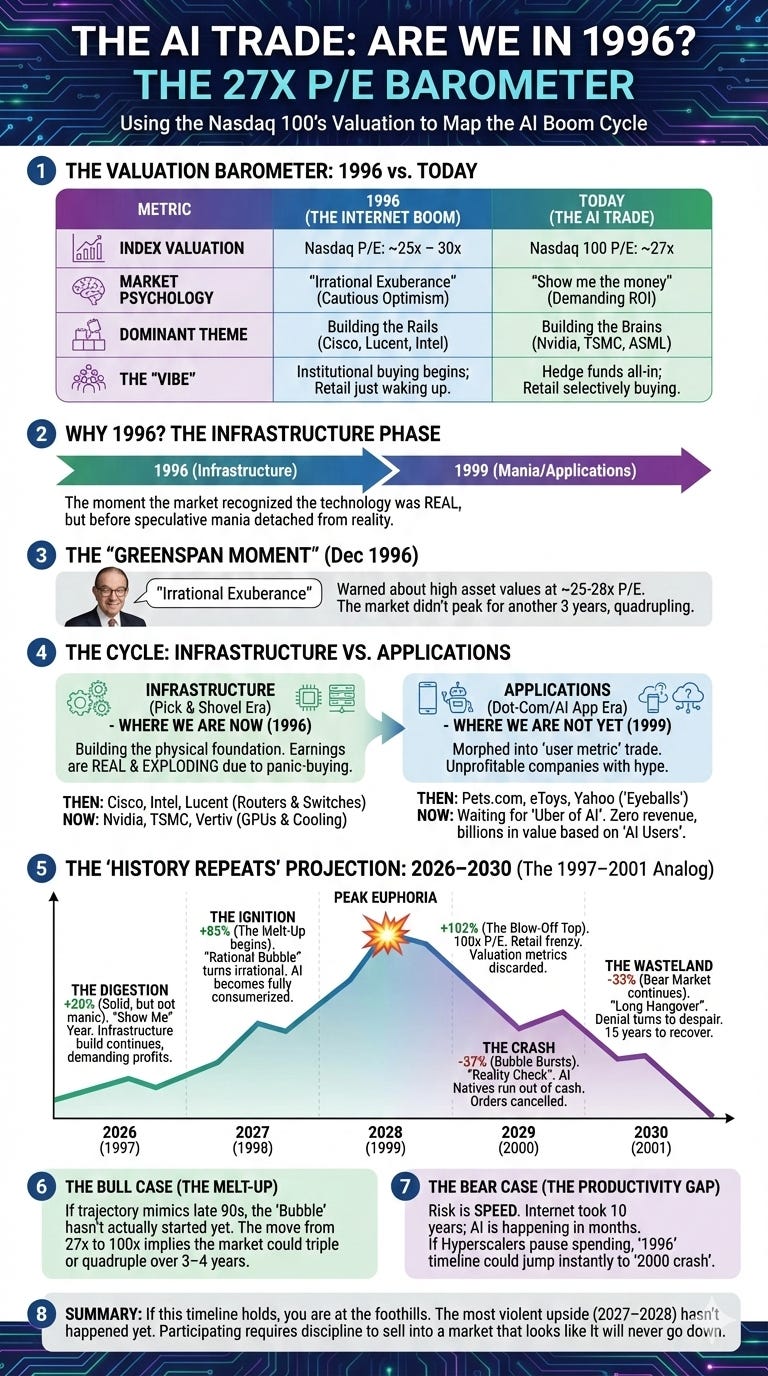

At that moment, the Nasdaq was trading at roughly 25 to 28 times its forward earnings. It was expensive by historical standards. It felt heady. It felt like too much, too fast. Greenspan’s warning was serious, sober, and rooted in data.

And the market completely ignored him.

Over the next three years, the Nasdaq didn’t crash. It quadrupled. The “irrational exuberance” of 1996 turned out to be merely the gentle slope before the mountain. The real irrationality, the moment when the market detached from gravity completely and hit 100 times earnings, didn’t arrive until March of 2000.

We find ourselves today, in January 2026, in a strangely similar ballroom.

We are witnessing a technological shift - Artificial Intelligence - that is demonstrably real. It is changing how code is written, how diseases are diagnosed, and how business is conducted. The companies powering this shift are not vaporware; they are titans with balance sheets larger than many sovereign nations.

Yet, because of this success, the tech-heavy Nasdaq 100 is trading at a forward price-to-earnings ratio of 27.

And just like in 1996, a chorus of sensible voices is asking the uncomfortable question: Are we in a bubble? Have we gone too far?

The answer, if you overlay the map of the last great technology boom onto today, is counterintuitive. Yes, we are in a bubble. But we are not at the end of it. We are barely past the beginning.

We are not partying like it’s 1999. We are just cracking the first beer in 1996.

To understand why, you have to understand the difference between the number 27 and the number 100.

A 27x multiple is what financial historians might call the “Infrastructure Phase.” It is a demanding valuation, yes. It assumes that companies like Nvidia and Microsoft will continue to grow earnings at 15% or 20% a year for the foreseeable future. It is a valuation that requires perfection, but it is rooted in arithmetic. We are building the rails, the data centers, the GPU clusters, the energy grid to power them. The spending is real, and the profits are immense.

A 100x multiple, where we were in 2000, is different. It is financial theology. It is the moment when investors stop doing math and start buying “eyeballs,” or “clicks,” or whatever metric happens to be in vogue. In 2000, the market wasn’t buying Cisco’s current earnings; they were buying a future that physically could not materialize fast enough to justify the price.

Today, we are still doing math. The math is aggressive, but it is math.

If the trajectory of the previous technology cycle holds true, and human psychology suggests it often does, the timeline forward is both thrilling and terrifying.

If today is 1996, then 2026 is likely to be the year of “The Digestion.” A year where the market catches its breath, demands proof of ROI from AI software, and perhaps trades sideways or up modestly.

But then comes the shift. Then comes the moment the infrastructure phase bleeds into the mania phase.

If history repeats, 2027 becomes 1998 - the year the melt-up begins. 2028 becomes 1999, the year of peak euphoria, where valuations detach from reality, retail investors quit their jobs to day-trade AI stocks, and the market doubles in a frenzy of FOMO.

And then, of course, comes 2029. The hangover. The year the music stops, just as it did in 2000, and the market sheds 40% of its value as it remembers gravity.

The mistake sensible people made in 1996 was assuming that because something was expensive, it couldn’t get more expensive. They underestimated the sheer velocity of a narrative once it captures the public imagination.

The danger right now isn’t that the AI technology is a mirage. The danger is that it’s real. And because it’s real, we will inevitably take a rational premise, that AI will change the world, and push it to an irrational financial conclusion.

Greenspan was right about the exuberance in 1996. He was just three years too early on the consequences. As we stand here in 2026, looking at a 27x multiple, it’s worth remembering: the most dangerous part of the bubble isn’t when it pops. It’s the part right before, when everyone is making too much money to care.