The “Picks and Shovels” of the AI Gold Rush Isn’t Just Chips; It’s Power

Can Bloom, boom in 2026? Bloom Energy that is (just to be clear)

Everyone knows the first rule of a gold rush: don’t dig for gold; sell the shovels. In the AI revolution of 2024-2025, the “shovels” have obviously been GPUs, propelling Nvidia to stratospheric heights.

But as we head into 2026, the trade is shifting. The bottleneck for AI isn’t silicon anymore, it’s electricity. And that is where Bloom Energy (BE) transforms from a speculative energy play into a cornerstone growth stock for the next decade.

Here is the bull case for why Bloom Energy is the smartest way to play the next phase of the AI boom.

The Problem: The Grid is Broken

To train a single large language model (LLM), you need thousands of GPUs running 24/7. These “AI Factories” consume as much power as small cities. The problem? The US electrical grid is ancient, congested, and slow.

Timeline to build a Data Center: 12–18 months.

Timeline to get a Grid Connection: 4–7 years.

Do you think tech giants like Oracle, CoreWeave, or Amazon are going to wait 5 years for the local utility to upgrade a substation? Absolutely not. They need power now.

The Solution: Power in a Box

Bloom Energy sells “time.” Their Solid Oxide Fuel Cells (SOFC) can be deployed in weeks, bypassing the grid entirely. They sit right next to the data center, turning natural gas (and eventually hydrogen) directly into electricity without combustion.

This isn’t just a backup generator; it is primary power. It is cleaner than the grid, more reliable (no outages), and most importantly, it is available today.

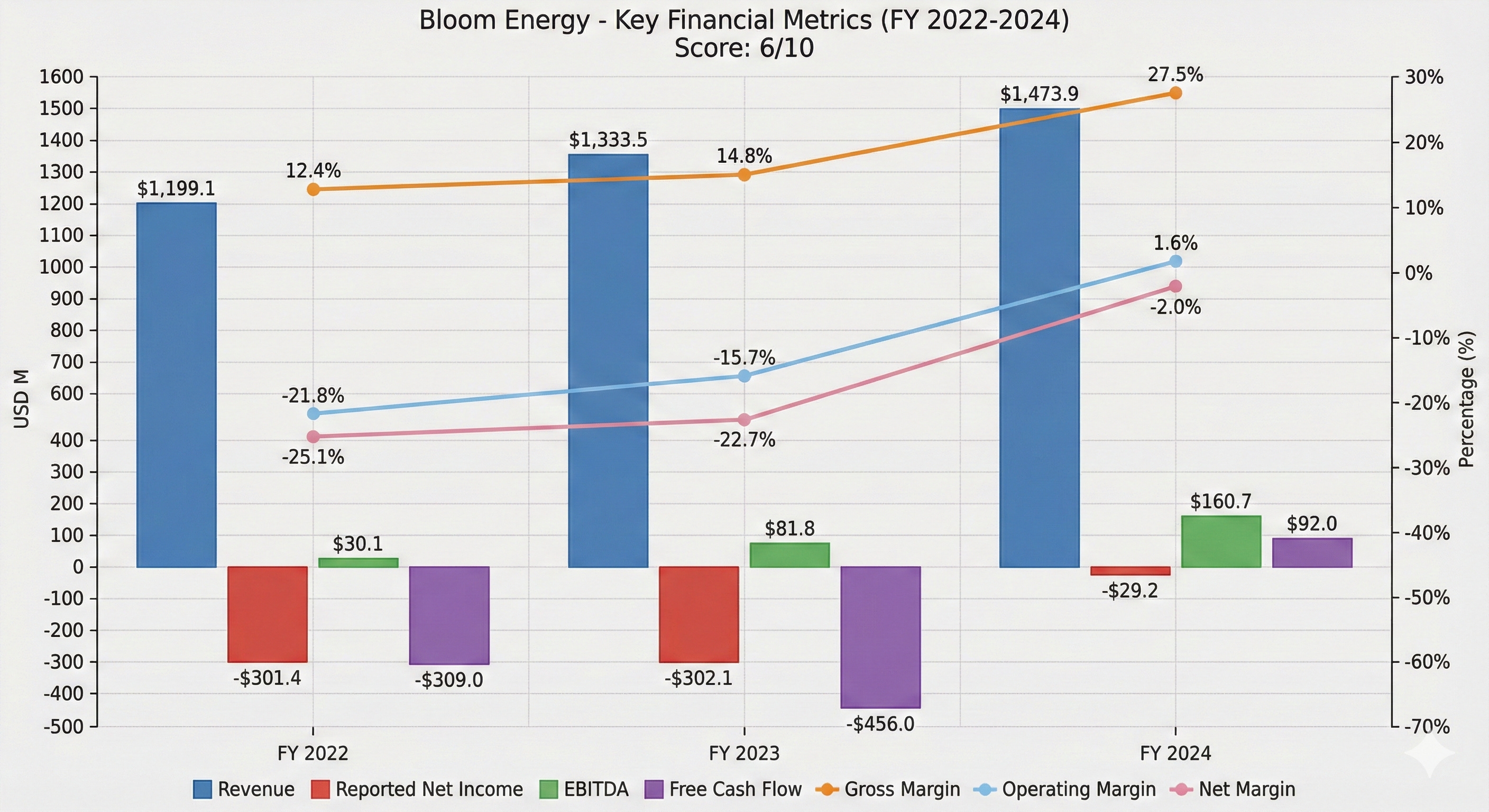

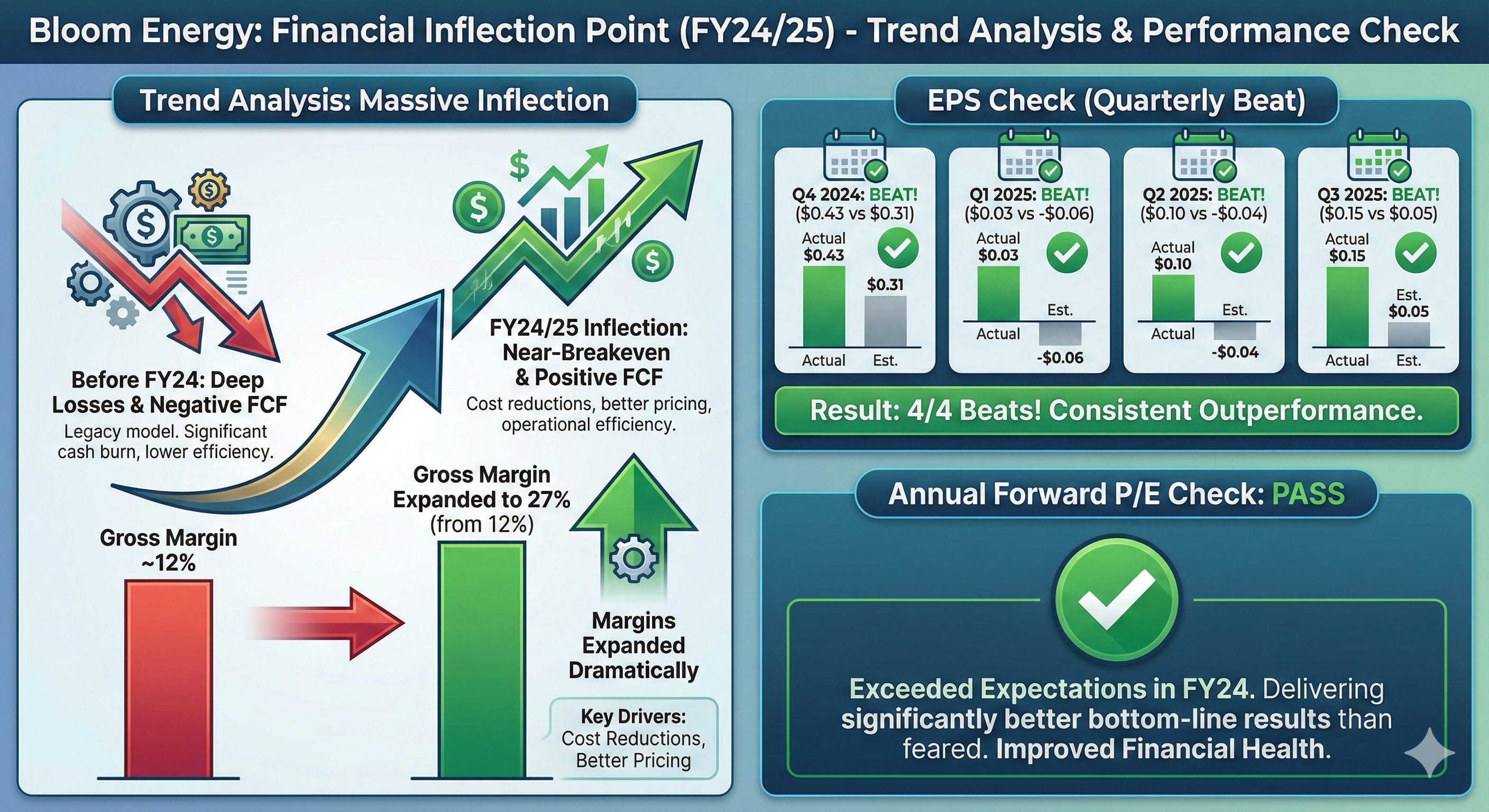

The Proof Is In The Numbers: Anatomy of an Inflection Point

Narratives get people interested, but numbers keep them invested. For years, the knock on Bloom Energy was that it was a “science project” that couldn’t stop burning cash.

If you look at the financial history, that criticism was fair, until 2024.

The graph below visualizes the massive financial inflection point that just occurred. This isn’t gradual improvement; it’s a step-change in business viability right as the AI demand wave is crashing ashore.

Here is what the data is shouting at us:

1. The Cash Burn Era is Over (Purple Bars)

Look at the purple bars representing Free Cash Flow (FCF). In FY 2023, Bloom incinerated $456 million. In FY 2024, they swung to positive $92 million in FCF.

That is a staggering half-billion-dollar turnaround in cash generation in a single year. This proves that Bloom is no longer reliant on endless capital raises to survive; the business model now sustains itself.

2. Pricing Power Has Arrived (Orange Line)

The orange line tracking Gross Margin is perhaps the most exciting metric for a growth investor. For years, margins hovered in the low teens (12.4% to 14.8%). In FY 2024, that line hockey-sticked up to 27.5%.

Why does this matter? It means Bloom isn’t just selling more boxes (Revenue, blue bars, is up steadily); they are drastically lowering their manufacturing costs while simultaneously commanding better pricing due to desperate demand from data centers. Doubling your gross margin is the ultimate signal of a maturing industrial company.

3. From Deep Red to Near-Breakeven (Red Bars)

While the company is still technically posting a small GAAP loss, the trajectory of Reported Net Income (red bars) is undeniable. They shrunk their losses from over $300 million a year to just $29.2 million in FY 24.

The takeaway: Bloom Energy spent a decade building a better mousetrap and bleeding cash to do it. The financial results from FY24 show that the R&D phase is over, and the profitable scaling phase has begun.

The “Smart Money” Signal: The $5 Billion Validation

If you need proof that this technology is ready for prime time, look at the money. In late 2024, Brookfield Asset Management, one of the world’s savviest infrastructure investors, signed a massive framework agreement to deploy up to $5 billion of Bloom’s fuel cells.

Brookfield doesn’t bet on science experiments. They bet on infrastructure that generates cash. This deal effectively standardizes Bloom’s technology as the go-to solution for off-grid AI power.

Why Buy Now? The “S-Curve” Inflection

For years, Bloom was a “show me” story that burned cash. But the fiscal data from 2024 and 2025 shows a company hitting its stride:

Positive Operating Cash Flow: They have stopped bleeding and started generating cash from operations.

Margins are Expanding: As volume ramps up with massive deals (like the 1GW agreement with AEP), economies of scale are kicking in.

The “Gigawatt Gap”: Estimates suggest the US faces a 35 GW power supply gap for data centers by 2030. Bloom is one of the few companies with the manufacturing capacity to fill it.

The Verdict

Bloom Energy is no longer just a “green energy” stock; it is an AI Infrastructure stock. It trades at a fraction of the multiples of the chipmakers, yet it solves the single biggest existential threat to AI scaling.

If you believe AI is going to keep growing, you have to believe power demand will skyrocket. And if power demand skyrockets, Bloom Energy is sitting in the pole position.

... Bloom Energy Just Pulled a Tesla — $5B AI Power Deal Explained ...

This video provides a great breakdown of the massive Brookfield partnership and explains why the financial “smart money” is finally treating Bloom’s technology as critical infrastructure rather than just a science project.