The Paper Monopoly: How a Single Paragraph Created an Aerospace Fortress

Embraer S.A. (NYSE: EMBJ)

The 86,000-Pound Clause

somewhere in the dense, litigious pages of the collective bargaining agreement between United Airlines and its pilots’ union, there is a clause that dictates the shape of the American sky. It is called the “Scope Clause.” It is boring, bureaucratic, and utterly decisive.

It stipulates that any aircraft flown by a regional partner (the cheaper airlines that feed the major hubs) cannot exceed 76 seats or a Maximum Takeoff Weight (MTOW) of 86,000 pounds.

If an aircraft weighs 86,001 pounds, it must be flown by “mainline” pilots, who cost significantly more. If it weighs 86,000 pounds, it can be flown by regional pilots, preserving the airline’s margins.

For the last decade, engineers at Mitsubishi in Japan and Bombardier in Canada tried to solve this equation. They failed. Mitsubishi incinerated billions on the SpaceJet before killing it. Bombardier exited commercial aviation entirely.

Only one company threaded the needle. Embraer S.A. (NYSE: EMBJ).

The Brazilian manufacturer’s E175-E1 is the only in-production aircraft in the world that fits this box. If you fly from Chicago to Des Moines, or Denver to Billings, you are almost certainly flying Embraer. Not because the airline loves Brazil, but because a single paragraph in a union contract gave them no other choice.

This is the “Micro” detail that explains the “Macro” truth: Embraer is not just a plane maker; it is a regulatory monopoly disguised as an industrial firm.

The Machinery: The “Negative Working Capital” Miracle

To understand how money moves through Embraer, you have to ignore the income statement for a moment and look at the way cash flows through an aircraft hangar.

In most businesses, you build a product (cost), put it on a shelf (inventory), and then sell it (revenue). Aerospace works backwards. Airlines are so desperate to secure their slots in the production line that they pay Pre-Delivery Payments (PDPs) years in advance.

When Embraer’s backlog grows—it currently sits at a record US$ 26.3 billion—cash floods into the bank account before a single rivet is driven. This creates a phenomenon called “negative working capital.” The customers are funding the operations.

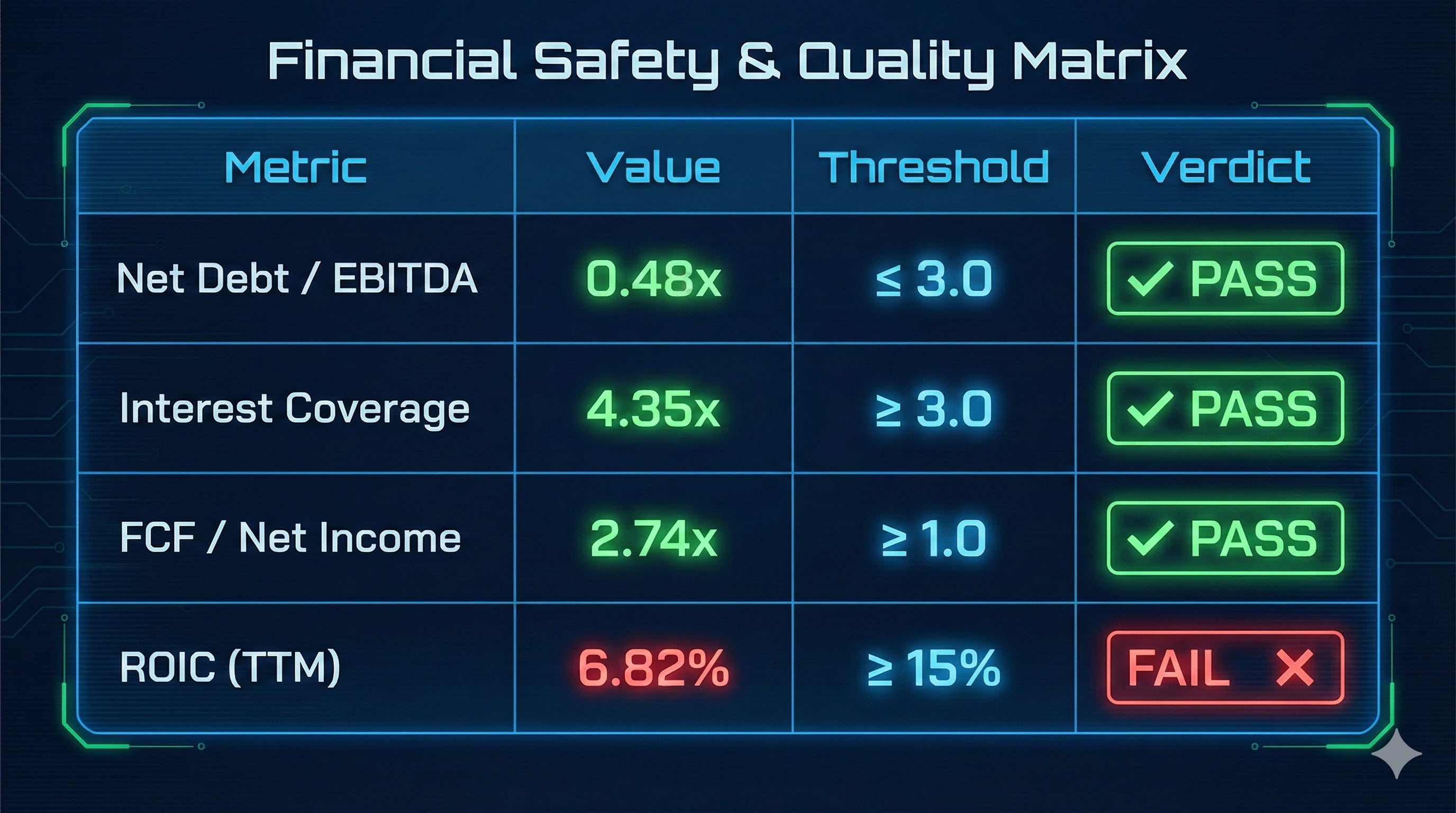

However, this machine has a friction point. Look at the financial safety checks below.

The Story in the Table:

Row 1 (Net Debt) is the headline. In 2021, Embraer was drowning in debt with a ratio near 4.0x. Today, at 0.48x, they are virtually debt-free in net terms. They used the influx of customer deposits to deleverage aggressively.

Row 4 (ROIC) is the warning light. A 6.82% return on invested capital tells us that while the company is safe, it is still capital-heavy. It costs a lot of money to keep the lights on in São José dos Campos. This isn’t a software company; it’s a heavy industry grinder.

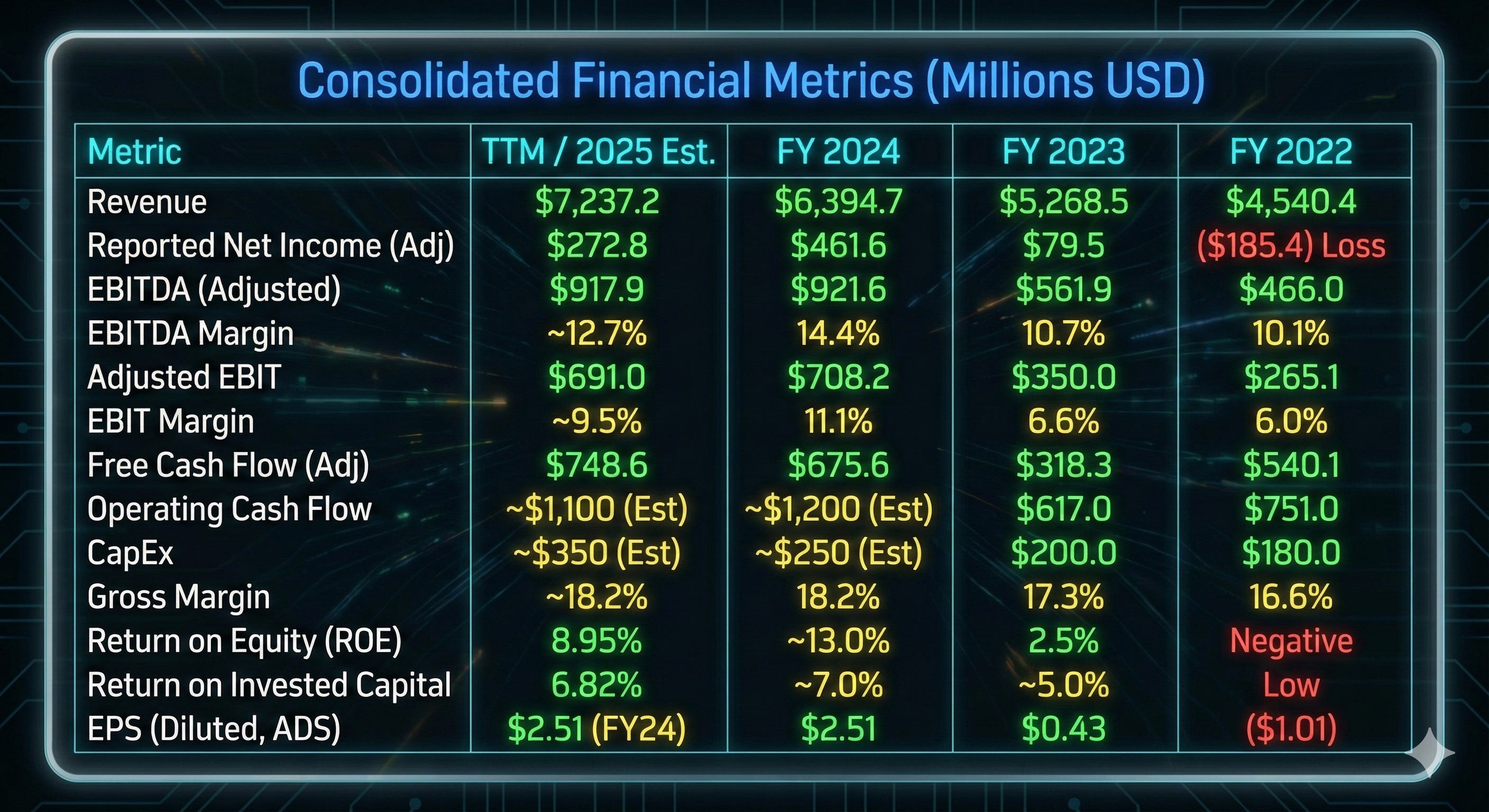

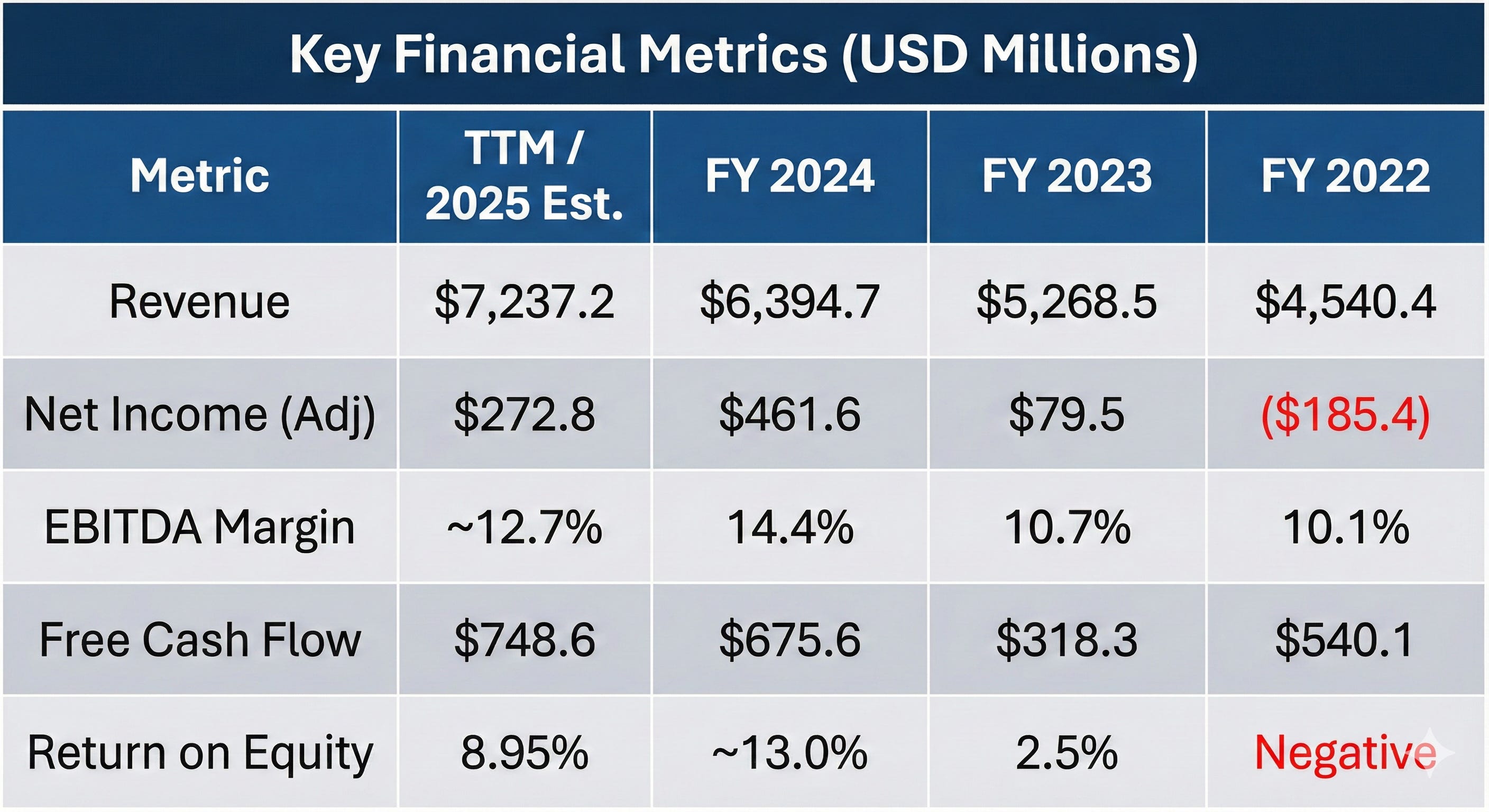

The Investigation: Forensic Analysis of the Comeback

We need to look at the granular breakdown of the last three years to see if the turnaround is structural or luck.

Exhibit A: The Profitability Pivot

In 2022, the company lost money (Net Income of -$185M). By 2024, they printed $461M in profit. This wasn’t just about selling more planes; it was about the “Toyota-fication” of their production line. Management reintegrated the commercial unit (which had been carved out for a failed merger with Boeing) and stripped out costs.

Exhibit B: The Cash Flow Mirage?

The TTM Free Cash Flow of $748.6 million looks incredible against a market cap of ~$12 billion. However, you must apply the skeptic’s lens. This number is inflated by the massive inflow of deposits (PDPs) for future jets. If orders slow down, this cash spigot turns off instantly.

The Bull Case: The David vs. Goliath Disruption

The optimist looks at Embraer and sees a company that has finally found a weapon to kill a giant. That weapon is the C-390 Millennium.

For 50 years, the Lockheed Martin C-130 Hercules has been the default military transport for the Western world. It is a turboprop designed in the 1950s. Embraer looked at this monopoly and built a jet-powered rival that flies faster (470 knots vs 310 knots), carries more cargo, and requires less maintenance.

The market assumed this project would die. Developing military hardware is usually a game for NATO insiders. But then, the Netherlands bought it. Then Portugal. Then Austria. Then South Korea.

The Bull Thesis:

The Defense Pivot: Embraer is transforming from a cyclical civilian manufacturer into a secular defense contractor. Defense contracts are sticky, long-term, and geopolitically mandated.

The Monopoly: The US pilot union “Scope Clause” isn’t changing. Embraer owns the US regional sky for at least another decade.

Eve Air Mobility: Embraer owns ~84% of Eve, a separate company building electric vertical take-off (eVTOL) taxis. The market is assigning almost zero value to this “lottery ticket,” but if urban air mobility works, this stake alone could be worth billions.

The Bear Case: The Valuation Trap

The skeptic looks at the share price and sees a classic case of “pricing in perfection.”

The Valuation Wall

At US$ 65.43, the stock has rallied over 76% in a year. Let’s look at the valuation reality:

Current P/FCF: ~16.2x

Intrinsic Value (Base Case): ~$41.43 per share (based on normalized cash flows).

The market is paying nearly $66 for a stock that the math suggests is worth $41. Why? Because the market is projecting straight-line growth into infinity.

The Supply Chain Choke

Embraer frames (the metal body) are ready, but the engines are missing. The industry is plagued by issues with Pratt & Whitney GTF engines. You cannot deliver a glider to an airline. Every delayed engine delivery creates a pile of inventory that burns cash and delays revenue recognition.

The “Good Enough” Problem

While the C-390 is a better plane than the C-130, military procurement isn’t just about specs; it’s about politics. Lockheed Martin has arguably the most powerful lobbying arm in Washington DC. For Embraer to win the “whale” contracts (USA, India, Saudi Arabia), they have to beat the politics, not just the physics.

The “Prime Target” Scenario

The “Grey Zone” Pullback:

If the broader market corrects or if a quarterly supply chain miss drives the stock down to the $38 - $42 range, the valuation realigns with the normalized intrinsic value. At that price, you are buying a monopoly business (Regional Jets) and getting a high-growth defense startup (C-390) for free.

The Strategic Catalyst:

Watch the Indian Air Force Medium Transport Aircraft (MTA) tender. If Embraer partners with an Indian firm (like Mahindra) and wins this contract, the Total Addressable Market (TAM) for the C-390 doubles overnight. A win there justifies the current premium. Until then, the price is speculation, not calculation.

Conclusion

Embraer has pulled off one of the most impressive industrial turnarounds of the post-COVID era. They have deleveraged the balance sheet, protected their moat, and built a better mousetrap in the defense sector.

But a great company can be a terrible investment if bought at the wrong price. Right now, the market has priced Embraer as if the C-390 has already conquered the world. The smart money waits for the inevitable supply chain hiccup to offer a better entry point.