The Alpha in the Alpine: How Amer Sports Engineered the Perfect Peak

Amer Sports (NYSE: AS)

The $200 Sneaker Anomaly

To understand why Amer Sports (NYSE: AS) is currently commanding a market capitalisation of $21.5 billion, you shouldn’t start by looking at the balance sheet. You should start by looking at the feet of a fashion editor in Paris, or perhaps a barista in Melbourne.

Specifically, look for the Salomon XT-6.

Ten years ago, this shoe was a niche tool for ultra-distance trail runners, a piece of ugly, aggressive plastic designed to survive mud and jagged rocks. It had zero fashion capital. Today, that same shoe sits on the shelves of high-end boutiques next to Balenciaga, selling for over $200. It hasn’t changed technically; the context changed.

This micro-anomaly is the key to unlocking the Amer Sports story. This is not a sporting goods company anymore. It is a machine that takes functional, unsexy engineering (ski boots, tennis rackets, rain jackets) and transmutes it into high-margin luxury lifestyle assets.

The market treats Amer like a manufacturer. But the data suggests it is morphing into a luxury holding company. And if you look closely at the third-quarter financials for 2025, you can see exactly where the alchemy is happening.

The Context: The “Gorpcore” Gold Rush

The global apparel market is currently split into two realities. In the middle, mass-market giants like Nike are fighting a bloody war of attrition, discounting inventory to move units.

But at the top, there is the “Gorpcore” (Good Ol’ Raisins and Peanuts) movement. This is the collision of technical survival gear and high fashion. In this reality, price is not a deterrent; it is a feature.

Amer Sports owns the crown jewels of this movement: Arc’teryx and Salomon.

In 2019, a consortium led by ANTA Sports (the Chinese sportswear giant) took Amer private. They didn’t just buy the brands; they bought the potential to strip out the “conglomerate” inefficiency and install a direct-to-consumer (DTC) supercharger. They returned it to the public markets in 2024, and now, in early 2026, we are seeing the results.

The Deep Dive: Following the Cash

Let’s stop treating the financials like a report card and start treating them like a crime scene. Where is the money coming from?

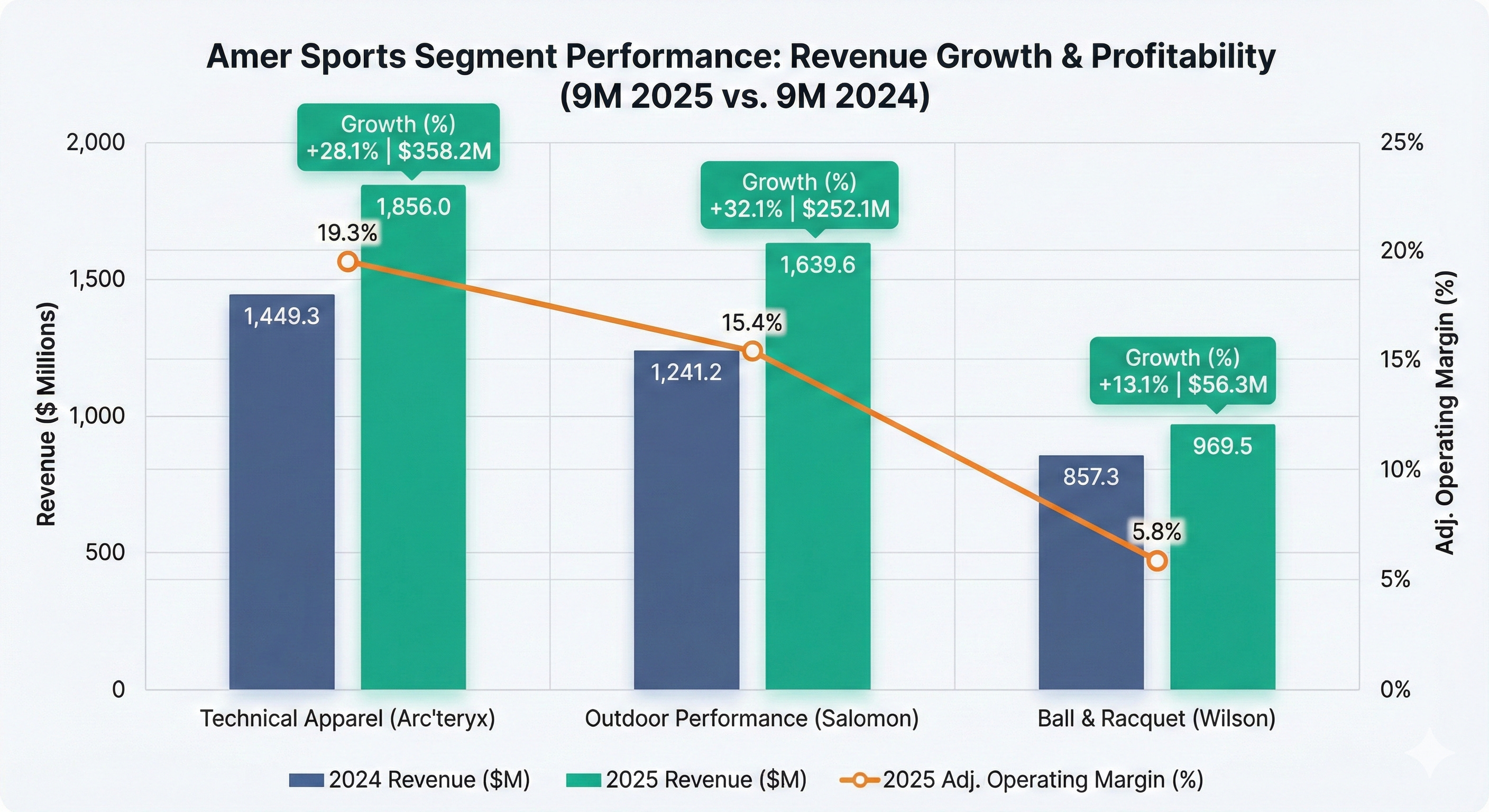

Below is the profit breakdown for the first nine months of 2025. Don’t gloss over this. Look specifically at the Outdoor Performance line.

Segment Profitability Analysis (9M 2025 vs 9M 2024)

Note: Total segment profit differs from consolidated operating profit due to corporate expenses.

The Clue: Look at the Outdoor Performance growth (+32.1%). This segment used to be seasonal, low-margin ski hardware (skis, bindings, boots). Now, it’s growing faster than the crown jewel, Arc’teryx.

Why? Because of the “Sneakerization” of Salomon. They are selling softgoods (high margin) instead of hardgoods (low margin). This shift drove the segment’s adjusted operating margin to a staggering 21.7% in Q3 alone (up 420 basis points).

The machinery here is obvious: Amer is successfully pivoting its legacy hardware brands into lifestyle software brands. They are selling the brand equity of the mountains to people walking on pavement.

The Bull Case: The “China Alpha” and the Veblen Effect

The optimist’s script for Amer Sports is not about selling more tennis rackets (They own tennis brand ‘Wilson’ who no longer has the assistance of Serena and Roger to help sell their racquets). It relies on three specific levers.

1. The Veblen Defence

Arc’teryx operates as a Veblen good, demand increases as price increases. An Alpha SV jacket costs $700+. In an inflationary environment, this is a superpower. While mass-market brands struggle to pass on costs, Arc’teryx customers are price-insensitive. The gross margin expansion to 57.9% in Q3 proves they have pricing power that rivals luxury houses, not sportswear companies.

2. The China Cheat Code

Most Western brands are bleeding in China. Nike and Adidas are losing ground to local patriots. Amer, however, has a secret weapon: ANTA.

Because ANTA is a major shareholder and strategic partner, Amer navigates the complex Chinese retail landscape with the agility of a local player.

The Data: Revenue in Greater China grew 47% in Q3 2025.

The Narrative: Amer is the only Western-facing luxury asset that effectively has “home court advantage” in the world’s fastest-growing consumer market.

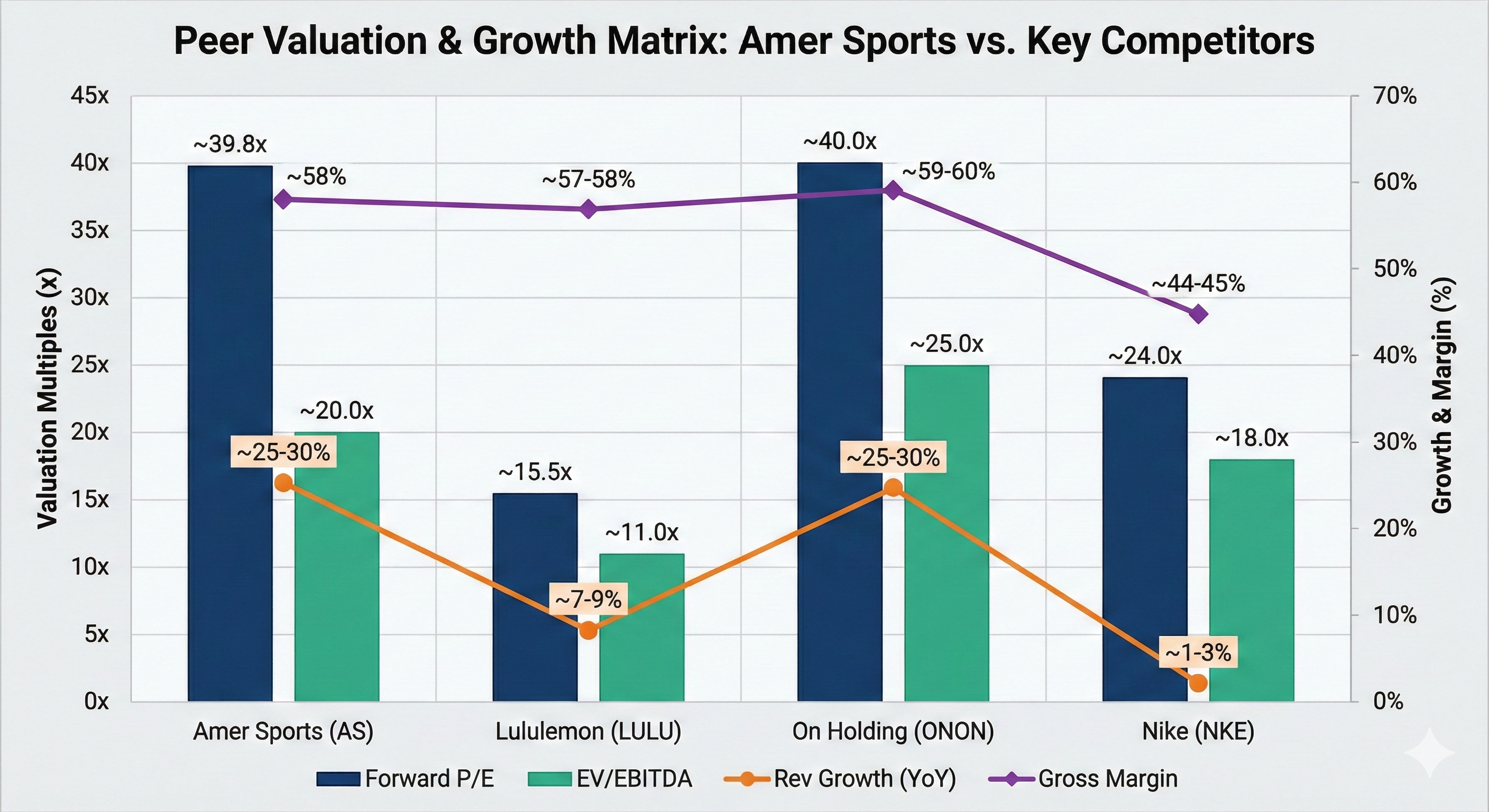

3. Valuation Relative to Growth

The market is pricing AS at a premium, but compare it to its peers.

Peer Valuation Matrix

You are paying a Nike-like multiple for On Holding-like growth. If Amer sustains 30% growth, today’s expensive price is tomorrow’s bargain.

The Bear Case: The Perfection Trap

The skeptic looks at the same data and sees a precarious house of cards.

1. Priced for Perfection

At ~65x TTM Earnings and ~25x EV/EBITDA, Amer Sports is priced for absolute perfection. If Arc’teryx growth slows from 30% to 20%, the multiple won’t just slide; it will collapse. The market is extrapolating a trend that is historically impossible to maintain indefinitely.

2. The Geopolitical Landmine

The “China Alpha” is also a single point of failure. The Bull Case celebrates the ANTA partnership; the Bear Case fears it.

The Incident: Remember the “fireworks controversy” in Tibet in late 2025? It was a minor blip, but it showed how quickly nationalist sentiment can turn against a brand.

The Risk: If trade tensions escalate or if Amer falls afoul of the UFLPA (Uyghur Forced Labor Prevention Act), nearly half of their growth engine (China) could be severed overnight.

3. The CapEx Heavyweight

Transitioning to DTC is expensive. You have to build the stores.

The Cost: CapEx is running at $300 million a year.

The Drag: This depresses Free Cash Flow (FCF). You aren’t buying this stock for cash returns; you’re buying it for capital appreciation. If the retail footprint stops generating high returns per square foot, Amer is left with massive fixed leases and a bloated balance sheet.

The Metric to Watch:

Watch the Inventory to Sales spread. Inventory grew 28% while sales grew 30%. As long as Sales Growth > Inventory Growth, they’re healthy. If Inventory Growth crosses above Sales Growth, the brand is cooling.

Conclusion

Amer Sports, looks like a sporting goods company, but it operates with the margins of a tech firm and the desirability of a luxury house.

They have successfully engineered a pivot that most legacy companies die trying to execute: turning utility into desire. With the balance sheet deleveraged (0.7x Net Debt/EBITDA) and the Salomon engine firing alongside Arc’teryx, they can keep walking the geopolitical tightrope without falling off.