The $390 Billion Bet on Second Place

Advanced Micro Devices: AMD

1. The Quarter-Inch Screw

In the back of a server rack, somewhere inside a hyperscaler’s data centre, there is a copper interconnect. It’s boring. It’s cheap. And right now, it is the most important piece of metal in the world.

To understand why Advanced Micro Devices (AMD) is currently trading at $240.34 a share, a valuation that implies the company will not just succeed, but conquer, you have to ignore the flashy marketing slides about “AI” and look at the wiring.

Dr. Lisa Su, AMD’s CEO, recently made a move that confused the casual observer but signalled everything to the insider: the acquisition of ZT Systems. ZT isn’t a chip designer. They are the people who figure out how to screw the racks together, manage the heat, and make the copper talk to the silicon. By buying them, AMD admitted a harsh truth about the modern semiconductor market: building the fastest chip isn’t enough anymore. You have to build the whole computer.

This is the story of a company trying to transcend its identity as a “chip designer” to become a “system architect.” It is a story of incredible engineering tension. But mostly, it is a story about a stock price that demands perfection in a world that rarely provides it.

2. The Context: The “Anyone But Nvidia” Trade

The market has decided that Nvidia cannot eat the entire world alone. The cloud titans, Microsoft, Meta, Google, are terrified of a single-supplier ecosystem. They are desperate for a viable alternative. They need AMD to win.

This desperation has fuelled a narrative that has pushed AMD’s market capitalisation to nearly $392 billion. The thesis is simple: The Total Addressable Market (TAM) for AI accelerators is so large (rumoured to be $400B+ by 2027) that even the runner-up gets rich.

But when you peel back the layers of the financial statements, a different picture emerges. It is a picture of a company fighting a war on two fronts: bleeding cash in legacy gaming while spending billions to ramp up a supply chain for a future that hasn’t fully arrived on the cash flow statement.

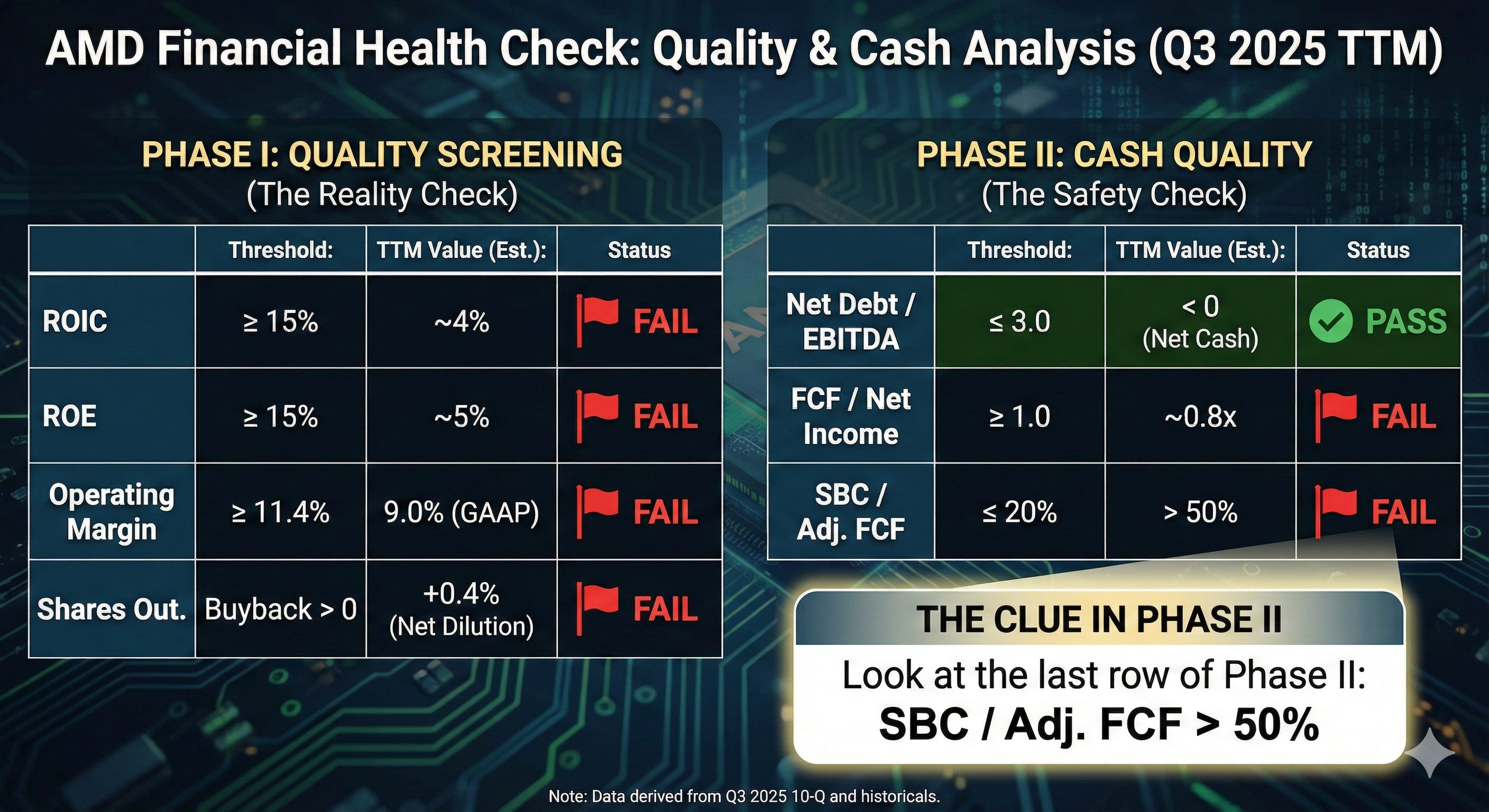

3. The Deep Dive: The GAAP Gap

Let’s look at the numbers. Not the “Adjusted” numbers the analysts love, but the raw, unpolished reality of the SEC filings.

If you read the headlines, you see a company growing comfortably. If you look at the below, you see a company whose valuation has completely decoupled from its current economic engine.

The Clue in Phase II

Look at the last row of Phase II: SBC / Adj. FCF > 50%.

This is the smoking gun. For every dollar of “Free Cash Flow” AMD generates, more than 50 cents is effectively promised to employees in stock-based compensation (SBC).

The company is paying its talent with equity to preserve cash for R&D. That is smart management, but it is expensive for you, the shareholder. You are being slowly diluted to fund the war effort.

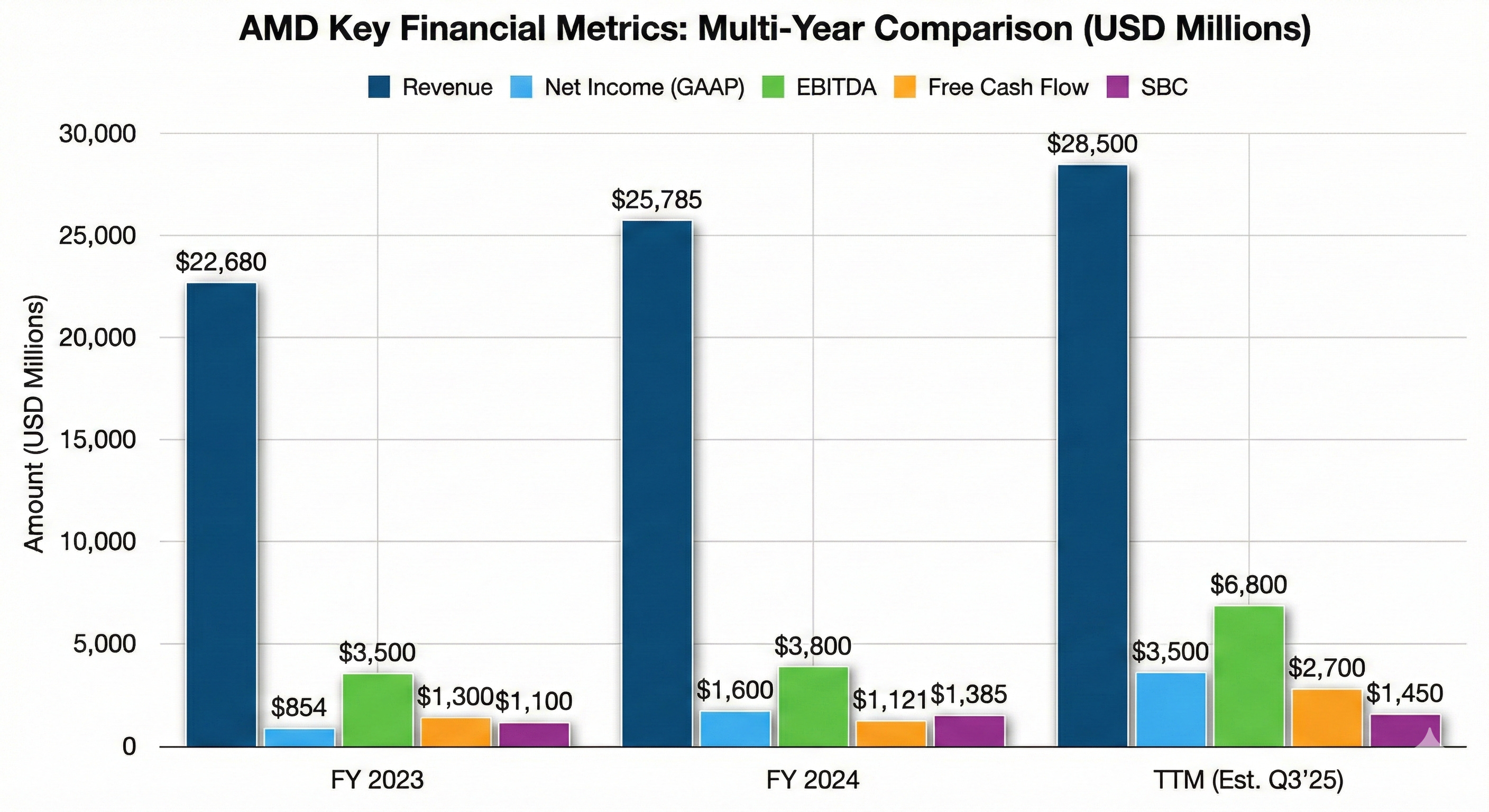

The Financial Trend

The table below shows the friction of the pivot. Revenue is up, but margins are fighting gravity.

The “Net Income” line looks great (doubling from 2024 to TTM), but the “Free Cash Flow” is lagging. Why? Because building AI chips requires massive upfront capital expenditure. AMD is buying inventory (HBM3e memory, CoWoS packaging) today for sales that happen tomorrow.

4. The Bull Case: The Blue Team’s Revenge

If you are buying at $240, you are buying a story of convergence.

The Argument:

The gap between Nvidia’s software moat (CUDA) and AMD’s alternative (ROCm) is closing faster than the market realises. The acquisition of Silo AI and ZT Systems proves that Lisa Su is fixing the software and hardware integration issues that plagued previous cycles.

Furthermore, the Data Center revenue is masking a cyclical bottom in PCs and Gaming. When the consumer cycle turns (and it always does) AMD will have its legacy engines firing alongside the AI rocket.

You aren’t paying 145x earnings for today’s company. You are paying for 2027, where AMD captures 20% of a $400 billion market. That’s $80 billion in revenue from AI alone. If that happens, today’s price looks cheap.

5. The Bear Case: The Valuation Trap

The Bear case is not about the technology; it is about the arithmetic.

The Argument:

The market is pricing AMD as if it has already won, yet the financials show a company still in transition.

The Xilinx Hangover: The massive amortization from the Xilinx acquisition suppresses GAAP earnings, making the P/E look artificially high. But even if you add that back, the price is steep.

The FCF Disconnect: You are paying nearly $392 billion for a business generating ~$2.7 billion in Free Cash Flow. That is a 145x multiple.

The Dilution Engine: With SBC running at >50% of FCF, the “owner earnings” are significantly lower than the headline numbers suggest.

The Bear sees a great company, but a terrible stock. They see a price that leaves zero margin of safety for execution errors, delay, or a sudden cooling in AI capex.

6. The Buy Trigger: When the Maths Work

We cannot buy a 145x FCF multiple. It violates the laws of financial gravity. However, AMD is a “wonderful business.” We just need a “fair price.”

The Scenario:

The “Buy” signal triggers in two scenarios:

The Price Capitulation: The stock needs to re-rate to a multiple where future growth isn’t fully priced in. If AMD retraces to the $150-$160 range, the risk profile flips. At that level, you are paying for the core business and getting the “AI optionality” at a discount.

The Cash Flow Inflection: We need to see Free Cash Flow cross $6 Billion TTM without a proportional rise in SBC. This would signal that the heavy capex cycle is over and the software margins are kicking in. Until cash flow matches the narrative, we wait.

7. Conclusion

AMD is currently a fascinating test of the “Second Shovel Seller” theory. The management is elite. The technology is viable. The customer demand is real.

But the price of admission is currently set for perfection. At $240.34, you are betting that the copper interconnects, the software stack, and the supply chain will all work flawlessly for the next five years.

For now, the story is better than the spreadsheet. And in this game, you never pay for the story alone.