The $2.5 Billion Ghost in the Machine

Coinbase Global, Inc. (COIN)

To understand the precarious brilliance of Coinbase Global, Inc. (COIN), you don’t look at the soaring stock price, and you certainly don’t look at the glossy marketing about “economic freedom.” You have to look at a single, boring, easily ignored line item buried deep in the machinery of their cash flow statement.

In the trailing twelve months leading up to September 2025, Coinbase reported a staggering Net Income of $3.2 billion. On paper, this is a company printing money. But if you trace the actual cash - the physical dollars moving through the pipes - you find a “Net Cash from Operating Activities” of just $326 million.

Somewhere between the profit statement and the bank account, nearly $2.5 billion vanished into the ether of “working capital adjustments.”

This specific anomaly is the skeleton key to the entire Coinbase story. It reveals a company that is technically profitable but structurally cash-inefficient, a “wonderful business” trapped in a valuation that assumes perfection while its own plumbing suggests something far messier.

The Survivor’s Premium

To appreciate why the market allows such a multi-billion dollar gap to exist between reported profit and actual cash, you have to zoom out. In the aftermath of 2022, when competitors like FTX and Celsius were exposed as little more than elaborate hall-of-mirrors frauds, Coinbase didn’t just survive; it became the default “adult in the room.”

But let’s be clear about the cost of that adulthood. While the live ticker tape flickers with the frantic energy of day-to-day sentiment, management set their own stake in the ground on 14 August 2025. To organise the $4.3 billion acquisition of the derivatives giant Deribit, Coinbase issued its own stock at a calculated fair value of $324.88 (a lot lower than today’s price).

This isn’t just a random quote; it is the “Deribit Anchor”- the internal truth of the company. It represents the price at which Brian Armstrong and his board were willing to dilute their own shareholders to buy future growth. When we talk about this $324 valuation, we are talking about the price of “Trust.” At this level, the market isn’t merely buying a crypto exchange; it is paying for a regulatory moat so wide and expensive that it has effectively become a tollbooth for the entire US cryptoeconomy. If you want to play by the rules, you pay the toll.

Yet, as we peel back the layers of the 2024 Annual Report and the Q3 2025 data before they report their 2025 earnings, the question isn’t whether Coinbase is a “wonderful business.” The question is whether even a fortress-grade tollbooth is worth a transactional multiple that currently defies the laws of financial gravity.

The Forensic Dive: Where the Money Goes

Let’s look at the engine room. The numbers below, pulled from the company’s recent filings, paint a picture of a business that is growing rapidly but bleeding efficiency.

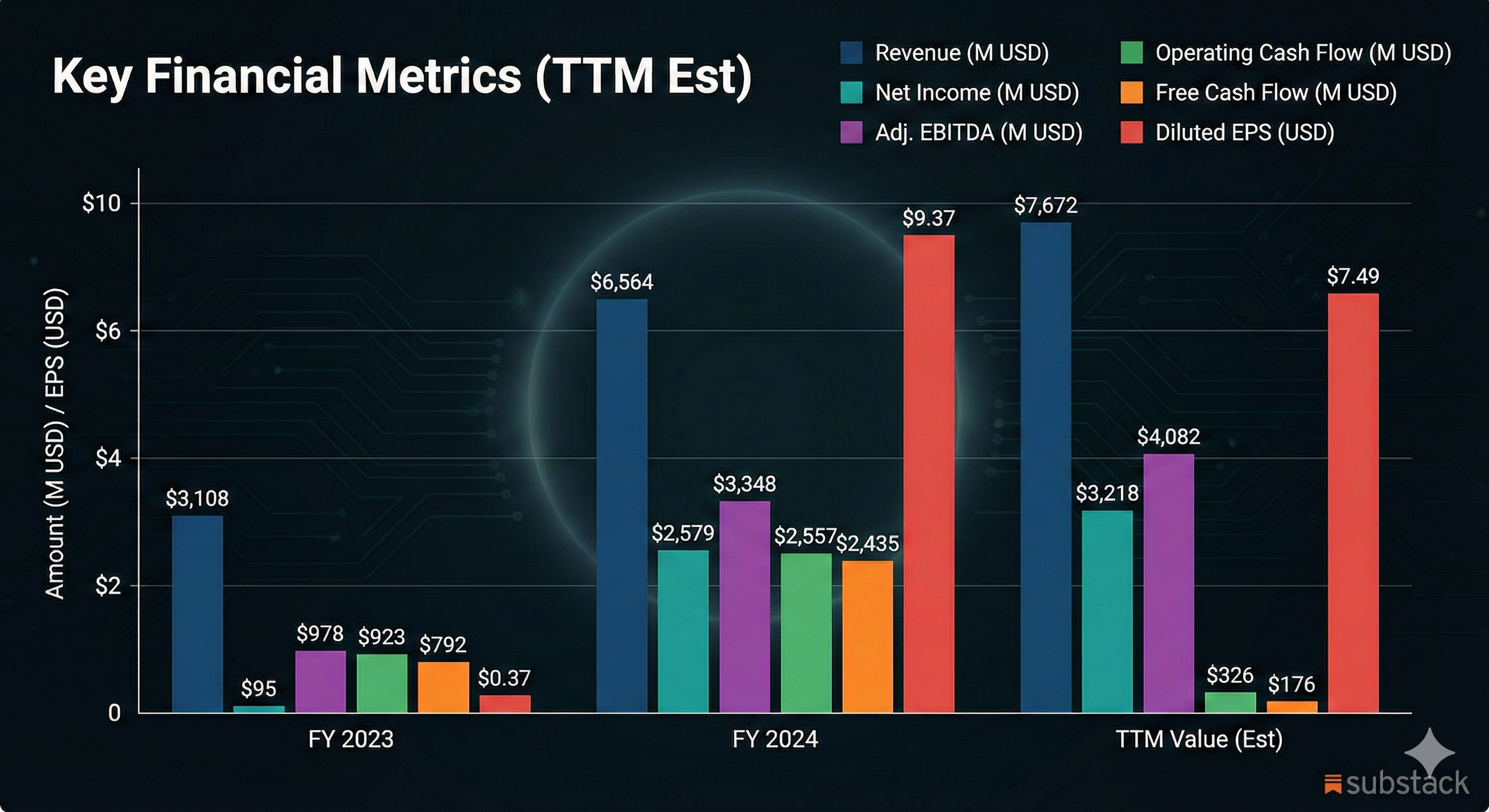

Key Financial Metrics (TTM Est)

The revenue growth is undeniable, more than doubling from 2023 levels. But look at the Operating Cash Flow. It collapsed from $2.5 billion in 2024 to $326 million in the TTM period. Why? A massive $2.5 billion outflow in “net changes in operating assets.” This often signals timing mismatches in settlements or massive increases in reserves (like USDC backing) that tie up cash. While not necessarily nefarious, it is a drag on liquidity that the “Net Income” figure conveniently ignores.

The Bull Case: The Amazon of Assets

The optimist looks at Coinbase and sees infrastructure, not just a casino.

The Diversification Play: Coinbase is successfully shifting away from pure trading fees (which are volatile) toward Subscription & Services revenue. This segment now includes stablecoin interest (USDC) and staking rewards, providing a predictable floor to their earnings.

The Base Layer: They aren’t just an exchange anymore; they are building a blockchain. Their L2 network, “Base,” is gaining traction with developers. If Base becomes the standard for on-chain apps, Coinbase owns the platform and the on-ramp.

International Aggression: The $4.3 billion acquisition of Deribit in late 2025 was a bold stroke. It instantly gave them a dominant position in crypto derivatives, a market far larger than spot trading.

In this narrative, Coinbase is building the railroads for the next century of finance. You pay a premium today because tomorrow, they will be the Visa, the NYSE, and the Swift network of the crypto world, all rolled into one.

The Bear Case: The Dilution Machine

The sceptic looks at the same numbers and sees a wealth transfer mechanism - from shareholders to employees.

The company’s Stock-Based Compensation (SBC) over the last twelve months was $879 million. To put that in perspective, the company generated $176 million in Free Cash Flow but handed out nearly a billion dollars in stock to its staff.

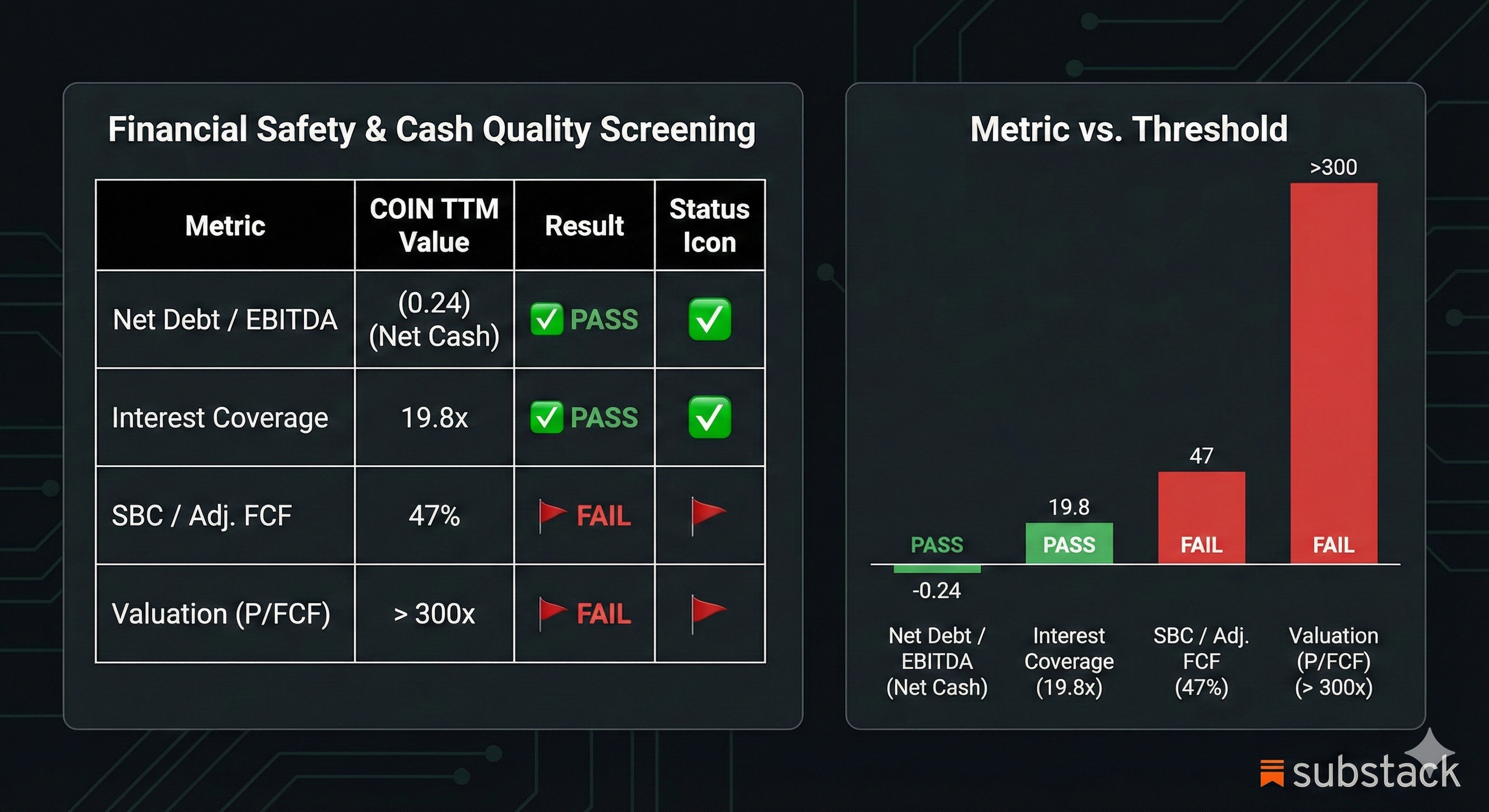

Financial Safety & Cash Quality Screening

The dilution is relentless. The share count swelled from 253.6 million to 268.7 million in just nine months. They used their inflated stock currency to buy Deribit, further watering down existing equity holders.

Furthermore, the valuation is disconnected from reality. Trading at 386x TTM Free Cash Flow, the stock is priced for perfection in a sector defined by chaos. The “Quality Check” matrix flashes red on almost every valuation metric. You are paying a luxury price for a business that is currently running primarily for the benefit of its insiders.

Conclusion

Coinbase has won the war for legitimacy. It has survived the regulators, the hackers, and the crypto winter. But winning the war doesn’t entitle a company to defy the laws of mathematics. Right now, shareholders are footing the bill for massive SBC and acquisitions while cash flow lags behind.

The story of Coinbase is one of immense potential masked by temporary inefficiency. The smart money sits on the sidelines, waiting for the “ghost” in the cash flow statement to resolve itself - or for the market to realise it has paid $325 for a $154 ticket.