The 100x Anomaly: Inside the 2026 Financial sector’s High-Stakes Poker Game

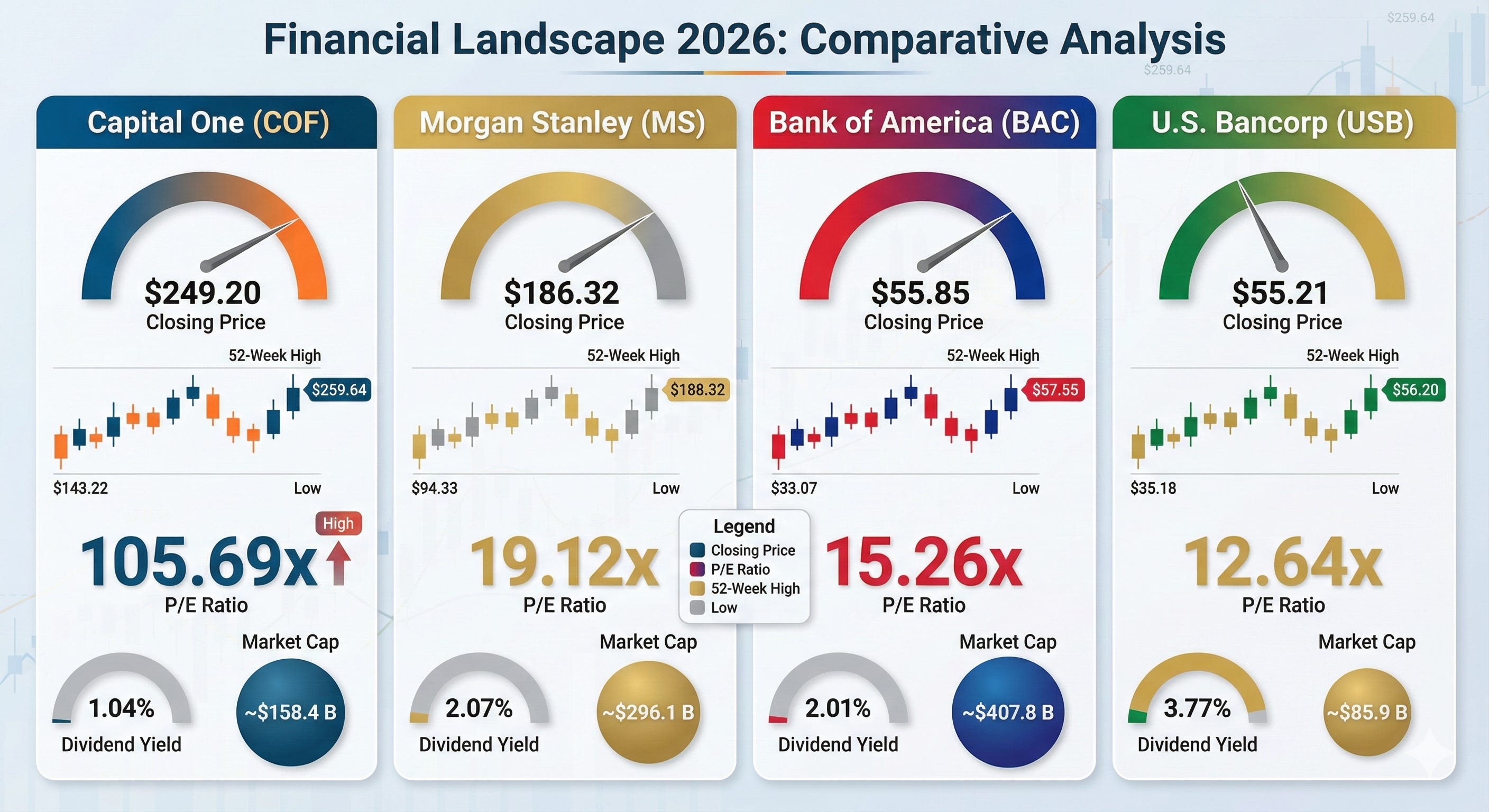

Capital One (COF), Morgan Stanley (MS), Bank of America (BAC), U.S. Bancorp

The Glitch in the Matrix

If you ran a screen on the S&P 500 financials sector on the morning of January 9, 2026, your eyes would have caught on a number that looked like a typo. Capital One Financial (COF) was trading at a Price-to-Earnings (P/E) ratio of 105.69x.

In a sane world, a bank trades at 10x or 12x earnings. A tech monopoly trades at 30x. A company trading at 105x is usually either curing death or about to go bankrupt. But Capital One is doing neither. That number, that distinct, ugly, three-digit outlier, is the single most important clue in American finance right now. It tells you that the old way of reading a bank balance sheet is dead, and a new, messier, high-stakes game of consolidation has begun.

Thanks for reading El’s Substack! Subscribe for free to receive new posts and support my work.

While the market obsesses over inflation prints, the real story of 2026 is happening in the plumbing of four institutions: Capital One, Morgan Stanley, Bank of America, and U.S. Bancorp. They aren’t just banks anymore; they are four distinct bets on how money will move in the next decade.

The Landscape: The Great Bifurcation

To understand, you have to ignore the indices and look at the divergent realities of the players. The market has split the sector into two camps: the Asset Gatherers (who are paid a premium for safety) and the Balance Sheet Bruisers (who are priced for disaster).

Here is the raw data from the close of trading on January 9. Don’t just skim it. Look at the gap between the dividend yields and the multiples.

The market is telling us two things here. First, it trusts Morgan Stanley’s fees twice as much as it trusts U.S. Bancorp’s loans. Second, nobody knows how to price Capital One, so they are pricing it on hope and accounting noise.

The Investigation: Dissecting the Four Pillars

1. Capital One (COF): The $400 Billion Closed Loop

The 105x P/E ratio isn’t a sign of growth; it’s a scar from surgery. Capital One spent 2025 swallowing Discover Financial Services. This destroyed their GAAP earnings via massive provisioning and integration costs ($348 million in direct expenses in Q3 2025 alone), artificially inflating the P/E ratio.

But if you strip away the accounting noise, you see the machine CEO Richard Fairbank is building. By acquiring Discover, Capital One is no longer just a bank issuing cards on someone else’s rails. They are now the issuer, the bank, and the network. They want to be American Express, but for the mass market.

The Clue in the Reserves:

Look at the Q3 2025 credit provision. It dropped by $8.7 billion sequentially.

Q2 2025: They hoarded cash, anticipating the worst from the Discover loan book.

Q3 2025: They released $760 million of that cash back into the wild.

This is the “tell.” Management looked under the hood of the acquired assets and realised the engine wasn’t as broken as they feared. The market sees this - the stock is up 74% from its lows - but the risk is now entirely political.

2. Morgan Stanley (MS): The Golden Handcuffs

Morgan Stanley is boring, and that is exactly why it costs $186 a share. Under James Gorman and now Ted Pick, the firm stopped being a casino and became a utility for the rich.

In the third quarter of 2025, they brought in $81 billion in net new assets. To put that in perspective, they essentially acquire a mid-sized regional bank’s worth of assets every few months, just by answering the phone. Their Return on Tangible Common Equity (ROTCE) is 23.5%. In the banking world, anything over 15% is good. Over 20% is elite.

The premium multiple (19.12x) exists because their revenue doesn’t rely on the vagaries of interest rates; it relies on fees. They are the landlord of American wealth.

3. Bank of America (BAC): The Sleeping Giant

If Morgan Stanley is a luxury yacht, Bank of America is an aircraft carrier. It turns slowly, but it carries heavy firepower. The narrative here has shifted from “balance sheet holes” to “operating leverage.”

The crucial data point is NII (Net Interest Income) Growth. For five consecutive quarters, NII has expanded, hitting $15.2 billion in Q3. The “cash sorting” panic—where customers pulled deposits to buy Treasuries, is over. With $1.99 trillion in deposits, BAC has won the war for liquidity. They are paying pennies for deposits and lending at 2026 rates. The math is inevitable.

4. U.S. Bancorp (USB): The Value Trap (That Isn’t a Trap)

U.S. Bancorp has been in the penalty box since it bought Union Bank. The market hates complexity, and that integration was messy. But the Q3 2025 spreadsheet suggests the punishment has outlasted the crime.

Efficiency Ratio: 57.2% (improving).

CET1 Ratio: 10.9% (rebuilt).

Yield: 3.77%.

This is the highest yielder of the group. The 12.64x P/E ratio implies the market thinks USB is a stagnant regional bank. The data, specifically the 9.5% growth in fee revenue, suggests it is a Payments powerhouse disguised as a lender.

The Narrative Tension: Two Realities

We are not looking for a “good company.” We are looking for a mispriced probability. To find it, we must weigh the Bull’s dream against the Bear’s nightmare.

The Bull Case: The “Soft Landing” was actually a “Launch Pad”

In this version of reality, the consolidation of 2025 worked.

For COF: The “Closed Loop” works. They move their debit volume to Discover rails, bypassing Visa/Mastercard. Margins expand instantly. The 105x P/E collapses to 8x as earnings catch up to price.

For MS: The wealth super-cycle continues as Boomers transfer trillions to Millennials.

For BAC/USB: The yield curve normalises. The “maturity wall” in commercial real estate crumbles harmlessly as rates settle, and these banks print money on the spread.

The Bear Case: The Political Sledgehammer

In this reality, the machinery breaks due to external force.

The Regulatory Kill Switch: The headline risk in January 2026 regarding a 10% cap on credit card interest rates.

This is the Bear’s ace card. If a 10% cap passes, Capital One’s business model, which relies on subprime and near-prime borrowers paying high rates, evaporates. Bank of America and U.S. Bancorp would survive, but their margins would be crushed.

The CRE Ghost: The commercial real estate crisis hasn’t hit the G-SIBs yet, but it’s rotting the floorboards. If unemployment ticks up, the office towers securing USB’s loans go from “distressed” to “default.”

The “Event-Driven” Buy

The safe money buys Morgan Stanley. It’s the treasury bond of equities.

The income money buys U.S. Bancorp. It’s mispriced and cheap.

But the asymmetric trade—the one where the “story” generates alpha, is Capital One (COF), but not at today’s price.

The stock is currently priced for perfection ($249.20). The market assumes the Discover integration generates billions in synergies. However, the political noise regarding the 10% rate cap is growing.

How would we Trade:

Wait for the headline: When the incoming administration formally proposes the rate cap legislation, algorithm-driven selling will hammer COF. It has the highest “regulatory beta.”

Watch the floor: If COF drops below $200 (breaking the 2025 support trends) on legislative headlines, the risk/reward flips.

The Logic: A 10% universal rate cap is politically unlikely to pass the Senate. The market will price it as a certainty; you will bet on gridlock.

At $200, you are buying the only vertically integrated payments network in the US (outside of Amex) for a valuation that ignores its strategic moat. You aren’t buying a bank; you are buying a payments technology firm that the market has temporarily confused with a subprime lender.

Conclusion

The spreadsheet is never just numbers; it’s a record of human behaviour. In 2026, behaviour has shifted toward scale. Morgan Stanley has won the wealthy. Bank of America has won the deposits. U.S. Bancorp has survived its surgery.

But Capital One is attempting to change the physics of the industry. It is the most dangerous stock on the list, both to own and to bet against. Keep your powder dry, watch the political headlines, and wait for the machinery to misprice the risk.

Thanks for reading El’s Substack! Subscribe for free to receive new posts and support my work.