Rocket Lab (RKLB): A Moonshot Business Priced for Perfection?

Ticker: RKLB | Price: ~$53.96 | Verdict: AVOID 🧨 but perception trumps value

Rocket Lab is undeniably building something wonderful. But is the price fair? Let’s dive into the numbers.

1. The Business Model: Simple and Ambitious

Rocket Lab’s business model passes the “Buffett Simplicity Test.” They do two things:

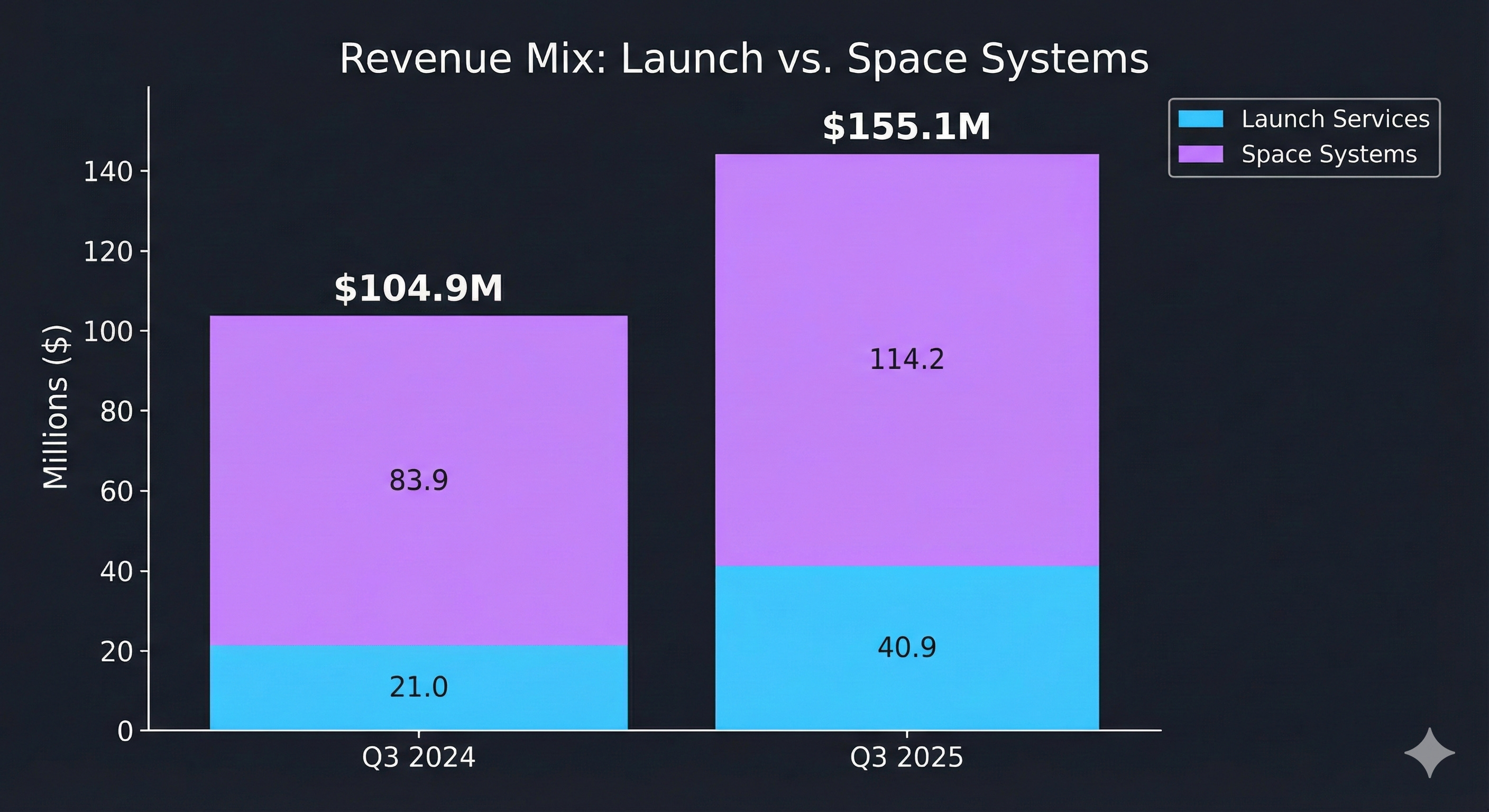

Launch Services: They launch satellites into orbit using the Electron rocket.

Space Systems: They build the satellites and components (solar panels, reaction wheels, radios) that go into space.

It is an “end-to-end” space company. They don’t just provide the taxi ride; they build the passenger, too.

2. The Moat: Technical Heritage

This is where Rocket Lab shines. The company possesses a genuine, widening moat built on technical know-how and heritage.

Track Record: As of September 2025, the Electron rocket has completed 68 successful missions. In the space industry, “flight heritage” is the only currency that matters. You either have flown, or you are a “paper rocket.” Rocket Lab has flown.

Vertical Integration: They own their own launch complex (LC-1 in New Zealand), which gives them control over their schedule that competitors sharing government ranges can only dream of.

The Next Step: Their moat depends heavily on the successful development of “Neutron,” a medium-capacity rocket designed to compete directly with SpaceX for larger constellations.

3. Management & Capital Allocation

At the helm is Sir Peter Beck, a visionary founder who was recently knighted and holds significant skin in the game (over 11% beneficial ownership).

However, from a capital allocation perspective, there are concerns:

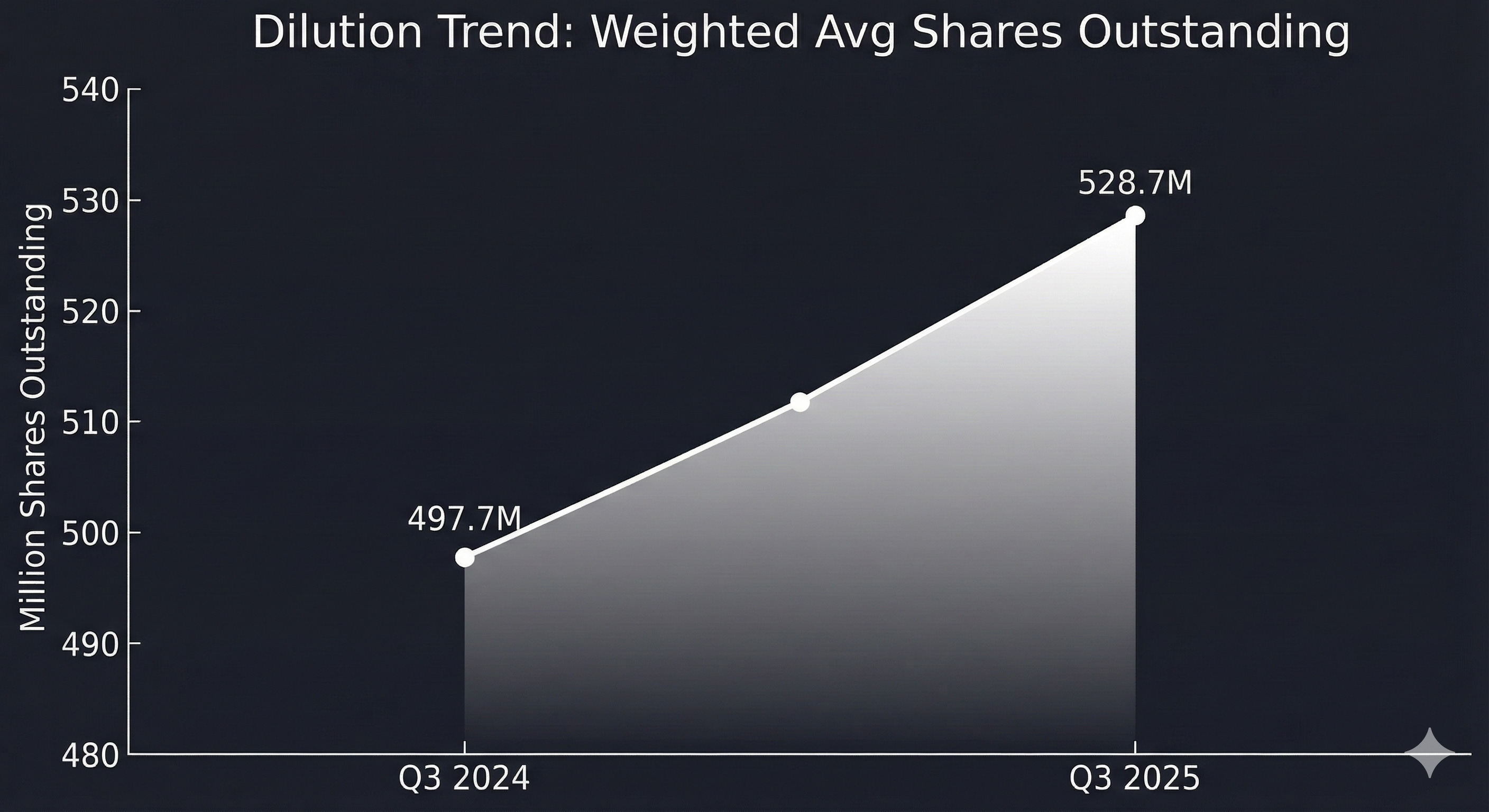

Dilution as Funding: The company funds its operations and capital expenditures largely through “At-The-Market” (ATM) equity offerings, raising over $865 million in nine months. This permanently dilutes existing shareholders.

Compensation Alignment: Until December 2024, the CEO had no long-term equity incentives. The board rectified this with a massive “catch-up” grant of RSUs, but the vesting is tied to time, not performance metrics like Return on Invested Capital (ROIC).

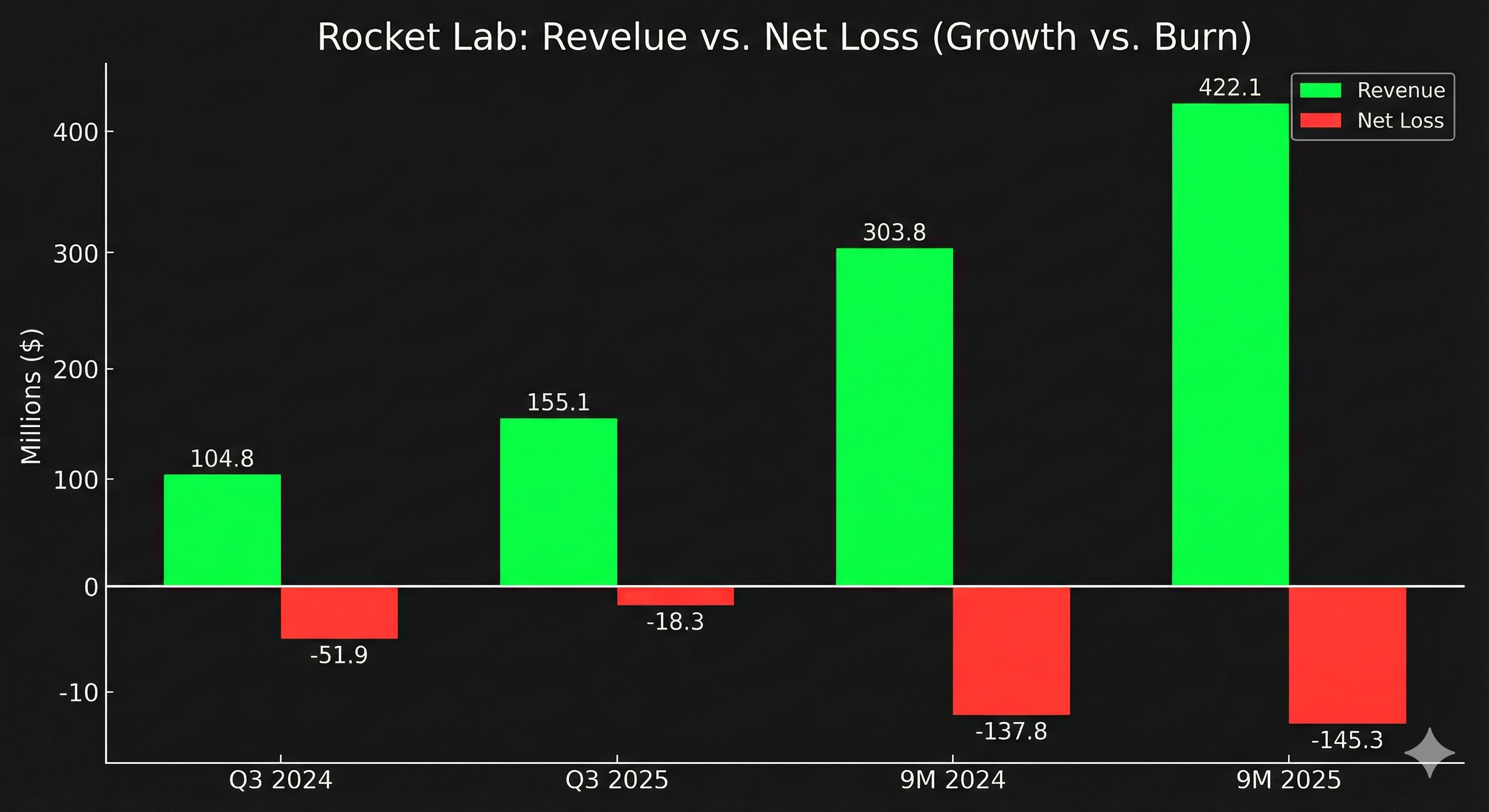

4. The Financials: Growth vs. The Burn

The income statement tells a tale of two cities: rapid growth and heavy losses.

Revenue is booming: Revenue grew 48% year-over-year in Q3 2025, driven by both higher launch cadence and satellite manufacturing.

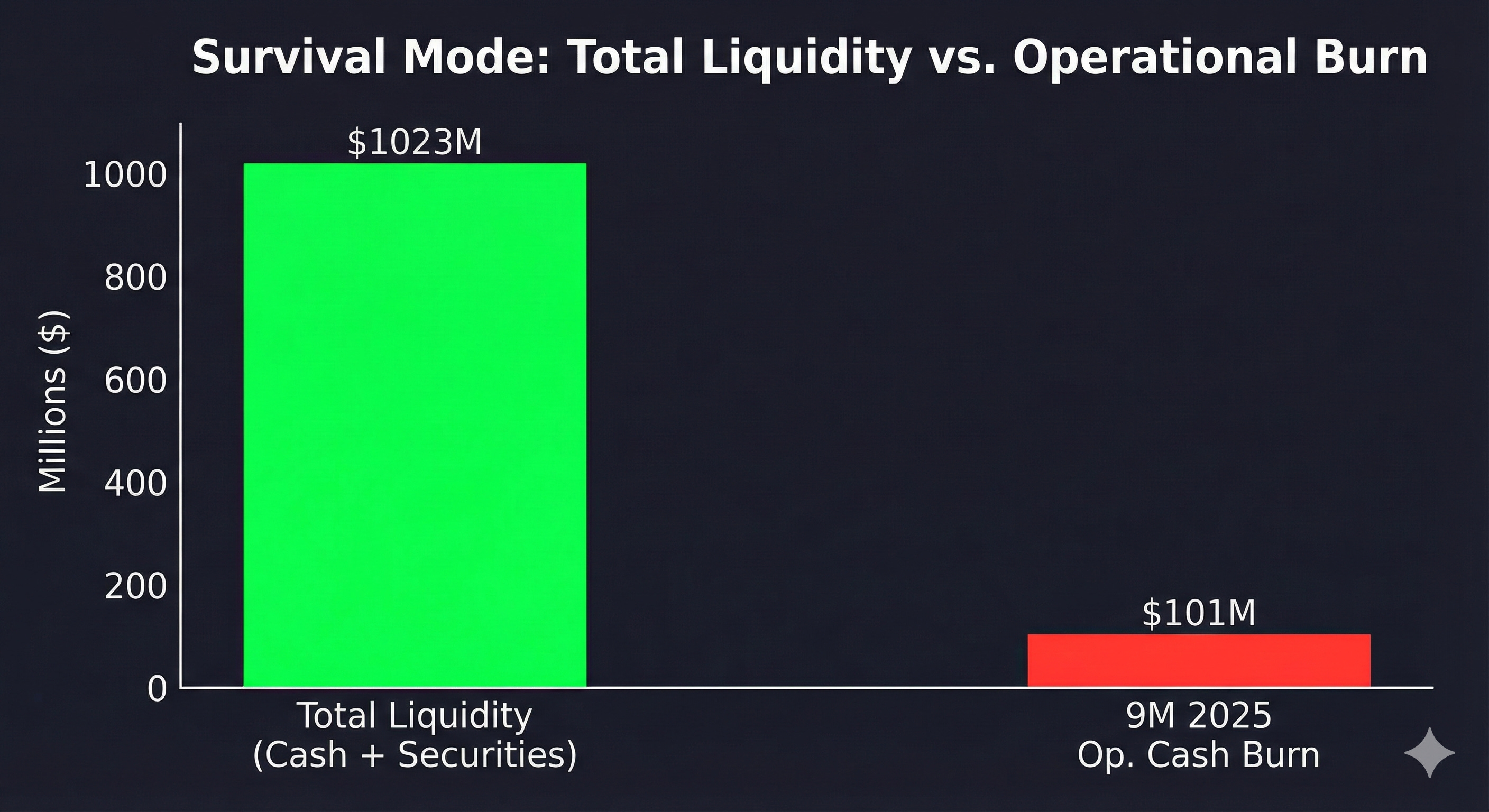

Cash is bleeding: Despite the revenue growth, the company burned $101 million in operating cash flow in the first nine months of 2025.

Stock-Based Compensation (SBC): A significant portion of their “operating” expenses is paid in stock ($52.9 million in 9M 2025), which suppresses cash burn on paper but hurts shareholders through dilution.

5. Debt & Risk Profile

Rocket Lab has a fortress balance sheet, but it comes at a cost.

Liquidity: They hold over $800 million in cash and equivalents. This provides a solid runway for developing Neutron.

The Debt: They carry $355 million in convertible notes and equipment financing.

The Risk: The entire investment thesis hinges on Execution Risk. If the Neutron rocket faces delays (a common occurrence in aerospace), the cash burn will extend, necessitating even more shareholder dilution.

6. The Valuation: The “Elephant Gun” Misfire

This is the dealbreaker. The Elephant Gun valuation model relies on Owner Earnings (Free Cash Flow adjusted for R&D and SBC).

Current Free Cash Flow: Negative ~$135M (3-year average).

Intrinsic Value: Because the company generates negative cash flow, the intrinsic value calculation returns $0.00 under standard value investing methodologies.

At a share price of ~$54.00, the market is pricing Rocket Lab not on what it is, but on what it might become years down the road. It is priced for absolute perfection.

7. Sentiment & Culture

Market sentiment is currently euphoric. The stock is trading near 52-week highs, driven by recent contract wins and U.S. Space Force missions. However, recent insider selling by the CEO (via 10b5-1 plans) casts a shadow over this peak valuation.

The Verdict: AVOID 🧨

Rocket Lab is a great company, but a bad investment at this price.

It passes the “Fisher” test (qualitative growth) but fails the “Graham” test (quantitative value).

The Good: Proven flight heritage, clear #2 player in launch, strong founder.

The Bad: Negative cash flow, constant dilution, and a valuation that requires flawless execution for years to justify.

Warren Buffett would say: “A great business, but we don’t pay for hope. Call us when the cash hits the register.”

🐘 My take: The SpaceX Multiple shows value ⭐️⭐️⭐️

Here is the counter-thesis that makes Rocket Lab compelling right now, despite the fundamentals: The SpaceX Halo Effect.

Recent reports indicate SpaceX is finalizing a tender offer at an $800 billion valuation and eyeing a potential IPO in 2026 at a staggering $1.5 trillion.

Let’s do the “napkin math” on what that means for Rocket Lab:

The SpaceX Multiple: With estimated 2025 revenue of ~$15 billion, an $800B valuation puts SpaceX at roughly 53x Sales.

The Rocket Lab Parity: Rocket Lab currently trades at a similar ~52x TTM Sales ($29B Market Cap / ~$0.55B Revenue).

The “Discount” Scenario: If SpaceX targets a $1.5 Trillion IPO, its multiple could expand to 75x-100x sales depending on growth rates. If Rocket Lab simply drafts behind this valuation expansion as the only liquid, public proxy for the space economy, the upside is significant.

At a 75x multiple (matching the SpaceX IPO hype), RKLB would trade near $75/share—a ~40% upside from here.

If Rocket Lab captures just 5% of SpaceX’s implied future value ($1.5T), that is a $75 billion market cap—nearly 3x today’s price.

Rocket Lab is the clear #2 in a winner-take-most industry. If SpaceX is the “Apple of Space” worth $1.5 Trillion, is it crazy to think the “Samsung of Space” is worth more than $29 Billion?

If you can stomach the volatility and ignore the cash burn, RKLB is a high-octane bet on the “SpaceX Economy” without the barrier of private markets.

Disclaimer: This is for informational purposes only and does not constitute financial advice. Do your own due diligence.