Lumentum - The Tollbooth at the End of the World: Buying the Infrastructure of the AI Boom.

How to Burn Cash and Influence Markets.

If you stare at the financial statements of Lumentum Holdings (LITE) for too long, you start to feel a familiar sensation: the urge to short.

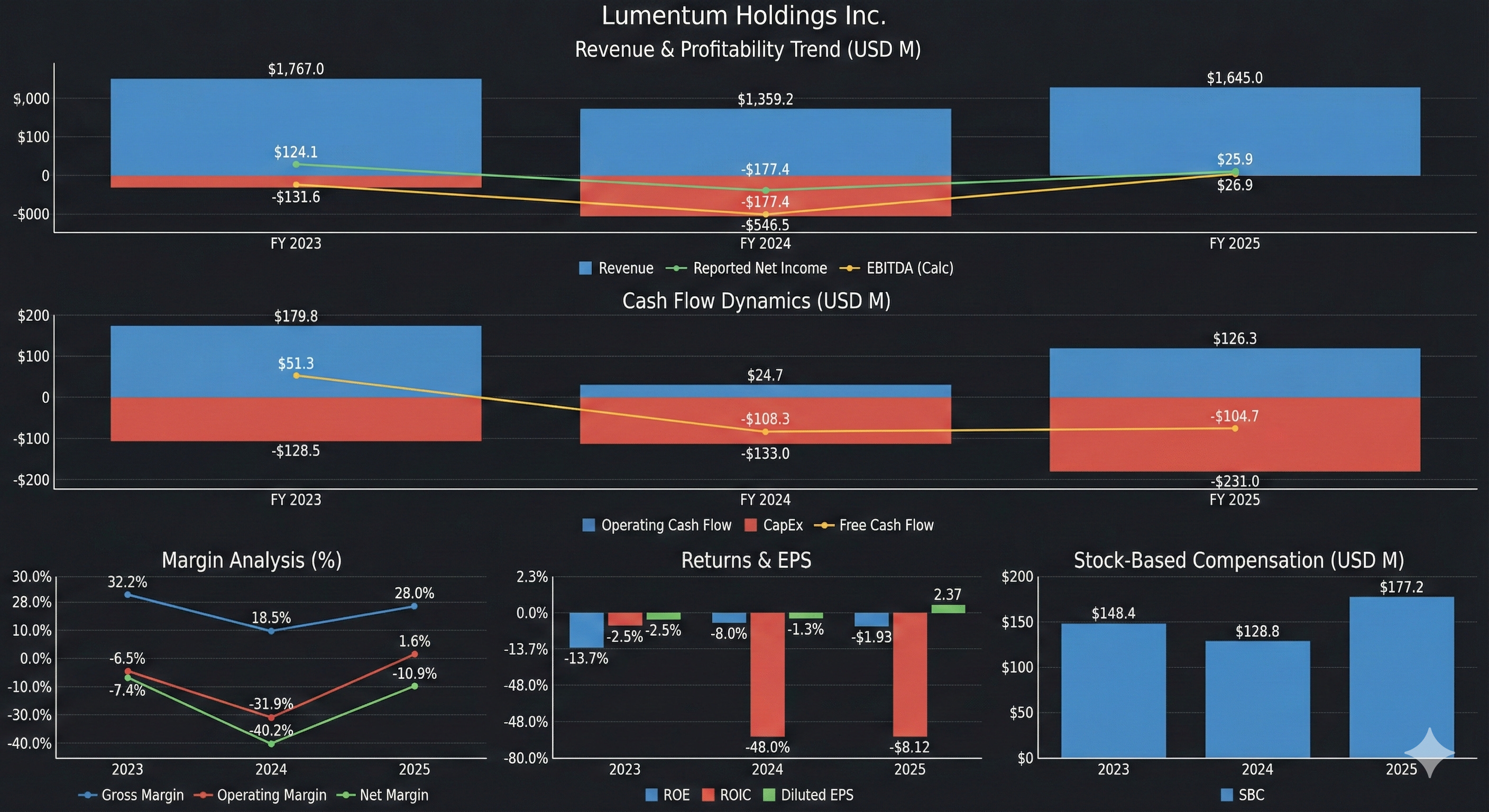

It’s all there. The bleeding income statement. The stock-based compensation - $177.2 million last year, that flows out of the shareholder’s pocket and into the employee’s driveway. The negative free cash flow of $104.7 million, which suggests that for every dollar of high-tech laser equipment they sell, they are essentially taping a dime to the box and mailing it to the customer.

On paper, trading at $386.11 a share, the company looks like a classic mania stock. It has $2.4 billion in debt, a leverage ratio that would make a junk bond trader sweat, and a bottom line that was only saved last year by a bizarre $198 million tax benefit.

But here is the thing about financial markets: sometimes the spreadsheet is the lie, and the story is the truth. And the story of Lumentum is the story of the one thing Silicon Valley cannot code its way out of: Physics.

The Speed Limit. Engineers vs Accountants.

To understand why a rational person might look at Lumentum’s messy financials and hit the “Buy” button, you have to ignore the accountants and listen to the engineers.

For the last twenty years, the internet ran on copper. Electrons moved through wires. It was cheap, it was easy, and it worked. But the Artificial Intelligence boom has broken the old world. When you ask a computer to “think”—to train a Large Language Model on the entire sum of human knowledge—you are moving data at speeds that turn copper wires into heating elements. If you try to run a modern AI data center on old-school cables, the signal degrades, the latency spikes, and the power bill bankrupts you.

The only way out is light. Photons.

This is where Lumentum lives. They make the microscopic tunable lasers and optical transceivers that turn electronic signals into pulses of light. They are the only reason the massive data centers being built by Microsoft, Google, and Amazon can actually function.

The Tollbooth of future intelligence

The bull case for Lumentum is not that they are a well-run manufacturing business today. It is that they are building a tollbooth on the future of intelligence.

When you look at that negative $104 million in cash flow, a value investor sees “cash burn.” A growth investor sees “moat building.” The company is pouring hundreds of millions of dollars into CapEx, factories, clean rooms, machinery, because they know what is coming. They are spending the money now to build the capacity that the hyperscalers will be desperate for in six months.

The debt? It’s high, yes. But if Lumentum is right, and they are one of only two or three companies on earth capable of mass-producing these optical chips at scale, that debt isn’t a burden; it’s leverage. It’s the cost of buying the table before the poker game starts.

The Invisible (but expensive) Asset

Then there is the “wasteful” Stock-Based Compensation.

In the niche world of photonics, there are perhaps a few thousand people on earth who truly understand how to dope indium phosphide wafers to create a laser that doesn’t melt when you run 800 gigabits of data through it. Lumentum employs a significant percentage of them. That $177 million isn’t just executive greed (though there is always some of that); it is the price of hoarding the only resource that matters: brains.

If Lumentum succeeds, that talent becomes the ultimate barrier to entry. You can give a competitor a billion dollars, but if they can’t hire the physicists because they’re all vesting stock options at Lumentum, the money is useless.

The Asymmetry

Caution: Ignore the above if you are buying 🙄

So, here is the wager.

If you buy Lumentum at $386, you are not buying a stream of cash flows. You are buying a call option on the physical infrastructure of AI.

If the AI boom is a bubble that pops next Tuesday, Lumentum is a disaster. The debt will crush them, the factories will sit empty, and the stock will go to zero.

But if AI is real, if the demand for data transmission continues to double every few months, then Lumentum isn’t just a supplier. They are a choke point. Eventually, the “Cloud & Networking” revenue, which already makes up 86% of their business, won’t just grow; it will explode. The pricing power will shift. When Amazon needs your lasers to turn on their $10 billion data center, you stop offering discounts.

The market hates Lumentum today because it looks ugly. It’s messy, expensive, and burns cash. But the smart money knows that the most profitable trades often look exactly like this right before they turn. They are betting that Lumentum is the ugliness before the dawn.